Issue #69: The Payments Sector Continues To Run Hot, Apparently Aussies Really 💜 BNPL And Coinbase Ditches Plans For Their Lend Product

Issue #69: The Payments Sector Continues To Run Hot, Apparently Aussies Really 💜 BNPL And Coinbase Ditches Plans For Their Lend Product

👋 Hi, FR fam. I hope you’ve all had a great start to the week.

Thanks as always for being a subscriber 🙌 Also, welcome to all the new subscribers — glad to have you here and welcome to the FR fold.

If you like what I’m up to with FR, please forward it to a friend or colleague. I’d really appreciate it!

Ok, without any further ado, let’s get into this week’s news from the world of fintech.

📣 The News Grab Bag

JP Morgan's UK digital bank is (apparently) ready for launch ⚬ QED announces another $1b+ fund to invest into fintech startups ⚬ Divining the real value of the BNPL segment ⚬ Bank has its OTP compromised. Ouch ⚬Curve to ‘flex’ its new BNPL product ⚬ Monzo also wants to get in on the BNPL action ⚬ DTCC Chain to go live in 2022 ⚬ Blomfield lifts the lid on foot-picking Softbank partner ⚬ UK Cardholder could own first-ever Mastercard NFT ⚬

📈 Notable Funding Announcements

It was a massive week of funding announcements in the world of fintech. In total, 74 funding rounds were announced, totalling $3.1b.

🧾 SpotOn Raises $300m at a $3.15b Valuation ⇢

This week PoS and payments focused startup, SpotOn, announced a $330m Series E that values the company at $3.15b — almost double the valuation of their May round of funding ($1.8b). The round was led by Andreessen Horowitz (who also led their Series D round of funding) with participation from existing investors, including DST Global, 01 Advisors, Dragoneer, and Franklin Templeton.

🤓 My Take: There’s been an under-discussed seachange in the world of PoS and merchant acquiring over the last ten years, which is now starting to produce some outsized outcomes for investors and customers alike.

For context, the segment was once a market dominated by merchant acquiring banks and an army of independent sales organisations (ISOs) that serviced specific industry verticals. Once upon a time, if you were a merchant, you’d need to have a direct and separate relationship with a bank (the merchant acquirer) and a software provider for your PoS. That changed around the time Square entered the market. Specifically, Square was one of the first, at scale, to show that working with a payfac that tightly coupled payments and the software you needed to run your business was a better option. Square ushered in a wave of companies that made it fast and easy to gets payments up and running for nearly every kind of merchant.

Since then, many players who started life as PoS providers adopted the Square model and tightly coupled their software and payfac offerings. The next significant change we saw in the sector was the expansion by these modern payfacs into being the operating system for their customer — offering working capital, SME banks accounts, payroll and even insurance. In fact, if you go to Toast's website, they clear call it out — “Point of sale was just the beginning”.

Like others in the market, SpotOn is playing a similar game. As noted in a recent article covering their recent raise, SpotOn is aiming to be the one-stop shop for businesses “…building a brand to taking payments and everything in between.” Their focus is slightly different from Square, Toast, Lightspeed et al., but the tactics are the same — providing the tools to run a business tightly coupled with the high margin business of providing payments.

It turns out PoS, especially in retail and hospitality, is an excellent wedge for fintech startups. For many SMEs, the ‘‘till’’ (whether virtual or physical) is the heart of their business — and many fintech servicing the SME segment have figured out the till provides a great vector of attack. Whether it's Toast and SpotOn in hospitality or Squire in hairdressing, many have realised that being at the heart of a company’s operations can be a great place to land and, importantly, expand from.

🤑 Xendit Raises $150m In A Series C Round Of Funding ⇢

Indonesian payments infrastructure company, Xendit last week announced a $150m Series C round of funding. The latest round of funding elevates the company to the shortlist of Southeast Asian fintech unicorns. The latest round was led by Tiger Global and had participation from their existing investors; Accel, Amasia, and Goat Capital.

🤓 My Take: Common wisdom in the world of fintech is that Stripe has won the market when it comes to being the payment processor of choice for digitally native companies. The reality is that in most markets, online payments are still dominated by local players. These companies tend to be hyper-focused on servicing the payment peculiarities of the markets they reside in with a tailored solution that makes sense in the context of that country.

In fact, if one were to construct a bear case for Stripe, it would begin with that Stripe is not a real player in the markets that are going to matter the most over the next decade — China, India and Africa (which is less the case now that they acquired Paystack).1 Beyond being regional focused, companies like Xendit in Southeast Asia and Flutterwave in Africa have also rapidly added new products to their offering. This isn’t dissimilar to what Stripe has done in the US, however in rapidly advancing markets, this is a crucial pillar of the offering as the options are usually limited, and the expectation is a company will act as a platform for all the services a business needs— after all Southeast Asia, in particular, is the home of the super. As Xendit's co-founder noted in a TechCrunch piece announcing the raise:

In Southeast Asia, you can’t just focus on one thing, you can’t just focus on payments. You want to focus on being this platform for every merchant to get onboard, and to never leave whenever they transact digitally.

Payments is a massive segment and highly fragmented not only by the product offering but also by geography. If you’re not deep in the payment pipes on a daily basis, it’s easy to disregard the amount that is happening on a global basis in the segment — that’s why monster raises like this on Xendit are a great reminder that many are still betting big on the opportunities in many of the emergent payments markets.

☝️ Things You Should Know About

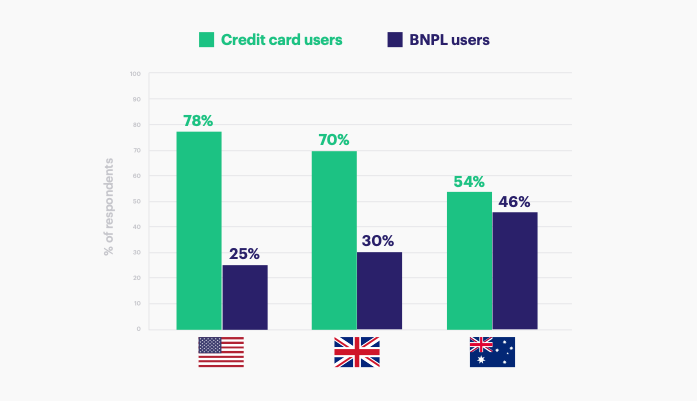

🇦🇺 Aussie Show A Strong Appetite For BNPL ⇢

It seems the data supports the view that Australia is the unrivalled home of BNPL. According to a survey run by Marqeta, Australians have increased their use of buy now pay later (BNPL) products during the pandemic. In fact, according to Marqeta, “three in four Australians have increased their use of buy now pay later (BNPL) products during the pandemic”.

Yes, the ‘survey data’ is only 1,000 people conducted by a company that recently signed a deal with ZIP (the second-largest BNPL player in the Aussie market) to be their card issuer of choice. Having said this, it feels like the data fall into the ‘unfair, but relevant’ bucket of data.

Anyone who’s been paying close attention to the Aussie credit card market knows it’s been falling off a cliff as people move from putting their purchase on credit to paying with the (gasp!) money they actually have in their account.

Directionally, the trend is clear, Australian consumers aren’t all that interested in using credit cards anymore. In many ways, timing has been everything for BNPL players in Australia as consumers look for other ways to defer payments that are less likely to result in debt spirals — yes, the data suggest most are linking their BNPL accounts to their debit accounts.

In Australia, directionally, it’s clear BNPL is on a tear, and it’s mainly driven by the move away from credit by younger consumers. It’ll be interesting to see what the catalyst is in markets like the US (if any) for more widespread adoption of BNPL.

🙅♂️ Coinbase Ditches Lend Programme After SEC Warning ⇢

Coinbase this week pulled the pin on its Lend, an interesting earning crypto product, after a very public scuffle with the SEC.

It all started with a tweet from Coinbase’s CEO, Brian Armstrong, who called out the SEC for some ‘sketchy behaviour.’

The tweet caused a bit of stir in crypto land as it again highlighted the challenges many crypto startups have been facing in the US. In summary, Coninbase was looking to launch a product that offered 4% APY on USDC held by a customer. However, after Coinbase approached the regulator with a heads up about the product, the SEC began to dig, resulting in a warning that if Coinbase were to launch the product, they’d find themselves in court.

The original tweetstorm suggested that Coinbase was ready to batten down the hatches and fight the SEC for clarity on why the product was in breach of the law. However, it seems that Armstrong and Coinbase have decided that this isn’t a fight they want to take on at the moment.

The crypto industry has been having a hard time with it in the US over the last few months, first with the now-infamous Infrastructure Bill and, more recently, with the SEC launching an investigation into defi darling Uniswap Labs. I’m sure this won’t be the last time we hear about a US regulator digging around in the sector. Regardless it’s clear the industry isn’t standing still as it tries to bring the defi mullet into existence — fintech in the front and defi in the backend (h/t Bankless).

🎧 Podcast Recommendations

Here are this week’s podcast recommendations. Enjoy👂

💳 Debit Karma ft. Poulomi Damany, GM of Credit Karma Money ⇢ This is another excellent episode of Tux Time from the team over at Fintech Today. In this episode, they chat with the GM of Credit Karma Money, Poulomi Damany, about their new product offering and why they decided to enter the crowded debit cards market.

🍪 Episode 446 Andy Taylor from Douugh ⇢ Douugh is an interesting case study in the Aussie challenger banking space. They elected to launch in the US vs in their home market after listing on the Aussie stock exchange (by way of a backdoor listing). In this interview, their CEO, Andy Taylor, discusses the challenger bank’s current offering and their future plans.

❤️ Show Some Love For FR

📈 You can check out Radar, an open database of Australia's fintech ecosystem. You can find it here → 📡 SideFund Radar

📧 Feel free to reach out if you want to connect. I'm me@alantsen.com and @alantsen on the Twitters.

Ps. If you like what I'm doing with FR, please feel free to share it on your social disinformation network of choice. I'd also appreciate it if you forwarded this newsletter to a friend you think might enjoy it.

🙏 What did you think of this week's issue of FR?

I love it! ◌ I Like It ◌ Not Bad ◌ I Don’t Like It ◌ It’s Awful