Issue #16: Fintech Listings, Web Browser Opera Acquires A Challenger Bank And What Banning Chinese Super Apps Could Mean For Fintech

Issue #16: Fintech Listings, Web Browser Opera Acquires A Challenger Bank And What Banning Chinese Super Apps Could Mean For Fintech

👋 Hi, FR fam. I hope the week is treating you well, and wherever you may be reading this email from you’re keeping safe.

This week saw another installment of fintech x ACNH, with Cash App running an in-game promo (h/t @dougatlast). It’s interesting to watch how effortlessly the Cash App marketing team seems to capture the zeitgeist of the moment with their promos — nicely done, Cash App.

💰 Notable Funding And IPO Announcements

Globally fintech financing was slightly down this week, with 36 funding announcements totalling $449m.

Instead of talking about capital raises this week, I thought I’d cover off on some of the listings and proposed listings in fintech land — and boy, there are a lot of them!

Ok, let’s start with the obvious. The window for IPOs has opened on the back of the NASDAQ going wild, and every company is running as fast as they can to the sill. It’s going to be a wild ride for the next few months as bankers work to get these deals off.

Arguably, the fintech sector has a lot of privately held companies that are primed to list. This has, in part, been exacerbated by the fact that private markets have been thrilled to plow money into the sector as it continues to grow — meaning there are some mature private companies ready to hit the NASDAQ ticker along with investors seeing this as the perfect time to get some liquidity.

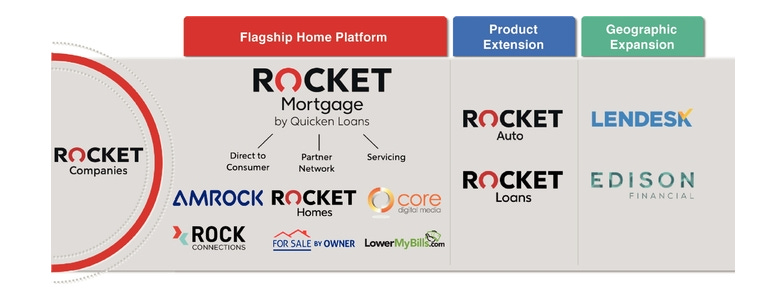

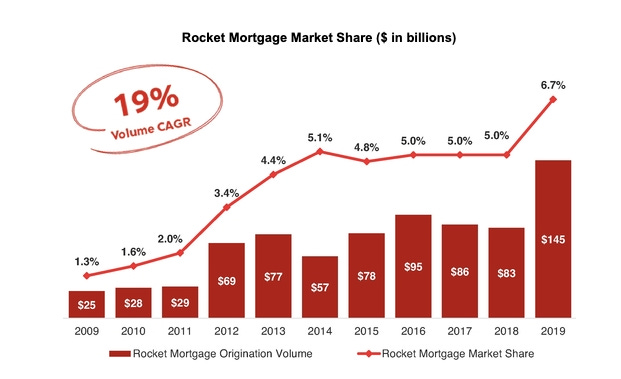

🏘️ Top U.S. Home Mortgage Lender Quicken Loans Files for IPO →

This is an S-1 many have been waiting to read. By way of background, the listing is for a portfolio of companies controlled by Rocket Inc (not just Rocket Mortgages) and includes a range of lending businesses that all sit under the Rocket Mortgage brand.

Rocket Mortgage has had a long and storied history under its enigmatic founder, Dan Gilbert — who incidentally is also the owner of the Clevland Cavaliers and is a co-founder of sneaker market place, StockX. The company is a well-known innovator in the digital mortgage origination business and is a commonly trodden out case study in the industry.

The S-1 tells an impressive story about the compounding growth the Rocket group of companies has seen over the last decade. Beyond this, they’ve also been able to generate annual profit for the past three years.

It’ll be interesting to see how financial markets price in the macroeconomic climate for lenders. In other words, let’s see how hard the Robinhood army YOLO trade this one 😜

⬆️ nCino Ups Its IPO To As Much As $253M →

A few weeks back, nCino dropped their S-1, and this week they decided to up the ante with an increase in the offering price to between $28-$29.

For some context for those who missed this one, nCino is a SaaS offering for FSIs. Specifically, they offer an operating system for client onboarding, loan origination, deposit account opening, and analytics. FSIs can use their products across several lines of business — it’s designed to be an all-in-one platform for the mission-critical operations a bank needs to serve its customers. In other words, it’s a highly verticalised CRM system designed explicitly for FSI.

The thing that has most intrigued me about their S-1 is that their whole product is built on top of Salesforce. Much like Veeva (who are a verticalised CRM for the life sciences industry and also wholly built on Salesforce), nCino is is another large and soon to be listed company that has been built on the Salesforce platform, which is in many ways mindblowing.

📈 Coinbase Looking At Listing →

Now, this would be one hell of a listing if it comes to fruition.

According to reports, Coinbase “has started plans for a stock market listing,” which could happen as soon as late this year. Moreover, the article also notes that they are looking to do a direct listing — meaning there could be some very fiat wealthy early employees of Coinbase when the company hits the NASDAQ ticker. Also, given that their last publicly announced funding round was in 2018(!) at a reported $8bn valuation, this could be a big payday for investors in the company. It’ll likely be a fund returner that will push a bunch of funds well into their carry.

🐜 Alibaba's Ant plans Hong Kong IPO, targets valuation over $200 billion→

Ant Financial is the unicorn of unicorns, with a valuation hovering around $150bn mark and it’s one of the most highly valued financial services companies in the world.

According to the article, the float would be done on the Hong Kong Stock Exchange and would value Ant Financial at $200bn valuation.

You may recall, Ant Financial shelved a planned IPO in 2019 and earlier this year resurrected their plans to dual list in mainland China and Hong Kong. This move away from a dual listing is an interesting new iteration on this proposed IPO. I can’t wait to see what happens next with this one — especially with all that is happening in Hong Kong at the moment.

💳 Marqeta Gets Ready To Go Public→

As discussed in issue #10, the payments sector is running hot, and this would be another much-anticipated listing.

As a quick reminder, Marqeta is a card issuing and processing platform that powers companies like Instacart, Square, Affirm, and Uber’s financial infrastructure. Earlier this year, they raised $150m at a $4.3bn valuation from some notable names, including Goldman Sachs and Visa.

Given the rise of embedded fintech (and Marqeta being one of the poster children for the plumbing supporting this movement), I could see this listing being met with a lot of excitement from many in the fintech community. I think investors in the fintech infrastructure space are probably champing at the bit to see the S-1 to better understand the underlying economics of this embedded fintech business — I know I am.

📰 Articles Worth Reading This Week

🏳️🌈 Mastercard Launches True Name Cards In Europe To Support The Transgender Community →

I thought this was a great initiative by Mastercard and something well worth highlighting.

According to the story, Mastercard is bringing it’s True Name cards to Europe. The True Card was initially launched in the US last year as a way for people from transgender and non-binary communities to have their chosen name displayed on their bank card.

A lot of the time, FSIs get a hard time for the way they treat their customers, but rarely do we highlight some of the positive work they are doing in the community. Nicely done, Mastercard!

🖥️ Web Browser Opera To Acquire Startup Digital Bank →

According to the article, the web browser, Opera, is going to acquire AB Fjord Bank. Many may not know this, but Opera has been recently eyeing off fintech offerings. For example, back in January of this year, they acquired Estonian fintech startup PocoSys - who is a BaaS provider.

On the face of it, this does seem like a strange acquisition. However, on the other hand, Opera’s browser is used by 360m people. In a world where financial services infrastructure is becoming commoditised, the real challenge is distribution - and Opera has a big channel it can hit if it wants to. Now, don’t get me wrong, there's a more nuanced question as to how they do that, but it’s worth keeping an eye on what they do with the Fjord Bank to see the approach they end up taking.

🏦 Fintech Disruptor SoFi Wants To Become A National Bank — Again →

According to reports, SoFi announced internally that they’ve applied for a national bank charter with the OCC.

Some of you may recall that SoFi submitted an application to the OCC back in 2017 but withdrew it’s application later that year after their then CEO, Mike Cagney, resigned amid allegations of sexual harassment. So the reapplication is probably not surprising to many. Further, it could also play into their strategy around expanding their lending book - as I noted in this piece regarding their acquisition of Galileo.

It’s also fascinating to watch how obtaining a national bank charter has become such a philosophical debate amongst challenger banks in the US (and for that matter globally). Personally, I’m keenly watching to see how the ‘be a bank vs. rent someone else infrastructure’ debate pans out.

🇨🇳 Banning Super Apps And It’s Potential Impact On The Fintech Sector

A few weeks back, the Indian government banned 59 apps developed by Chinese companies over concerns that they were “…engaged in activities which [are] prejudicial to [the] sovereignty and integrity of India, defence of India, security of state and public order”.

Amongst the apps that were banned, and most notably, was TikTok. However, the long list of blacklisted apps also included commerce apps like Clubfactory and super app WeChat. The treat of banning many of these Chinese apps in other countries has been a point of discussion for a while, and it’s looking more and more likely that other countries will follow India’s lead.

As most FR readers know, many Chinese apps also carry store of value functionality embedded in them. For many, the Chinese ‘super apps’ are the primary way they interact with the financial system. The banning of these apps, as they get caught up in the looming China vs. US cold war is going to be an interesting twist in the tale for many of these companies’ international growth plans. Most of the big Chinese super apps have pushed hard and fast into other markets through partnerships with banks and payment providers. It’ll be interesting to see if governments will more closely scrutinise these relationships along with their data collection practices.

It’s also interesting to reflect on some of the concerns other market players initially voiced when these players started to aggressively enter markets like the US. In this Bloomberg article from back in 2018, the concerns over how some Chinese super apps might undercut intermediaries in the US financial system were well highlighted. Although practically, these were no more than an existential threat to these intermediaries, I’m sure many will be sleeping a little easier if these apps end up on the blacklist of countries who decide to enact bans.

Don’t Forget…

📈 You can check out Radar, an open database of Australia's fintech ecosystem. You can find it here → 📡 SideFund Radar

📧 Feel free to flick me an email if you have any exciting news you'd like me to share with the FR community. I'm me@alantsen.com and @alantsen on the Twitters.

Ps. If you like what I'm doing with FR please feel free to share it on your social disinformation network of choice. Also, I'd appreciate it if you forwarded this newsletter to a friend you think might enjoy it.