Break Down #3: Fintech Trends From Q3 2020

Break Down #3: Fintech Trends From Q3 2020

Data for Q3 2020 is out, and in this issue of the Break Down, I go through the key fintech trends that emerged during the quarter.

👋 Welcome to this week’s issue of the break down! In this weekly missive, I dive into topical/ interesting/ under-discussed areas of fintech and provide you with a break down of what’s going on. There'll be lots of opinions and data, so get ready to nod in agreement, disagree, and in some instances, comment in ALL-CAPS about how vehemently you disagree with me (which you can do below in the comments section below 😀 ).

Don’t forget, if you enjoy this newsletter, make sure you share it with a friend - remember, sharing is caring!

I know Q3 is well and truly behind us and we’re now almost halfway through Q4, but I finally had a chance to sit down and read through all the summaries of Q3 financing activity in fintech and thought I’d share my notes with the FR fam.

⏪ A Quick Rewind To The First Half Of 2020

If you cast your mind back to the start of 2020 (which feels like it was 3 years ago), fintech started the year white-hot with some hot and heavy M&A activity. Deals like Visa buying Plaid, Intuit buying Credit Karama, and Morgan Stanely acquiring E*Trade were all signals that this was going to be another great year for the fintech M&A. Many investors licked their lips and readied those “we have some exciting news to announce” emails for their LPs.

Then COVID19 hit, and all bets were off.

We quickly saw investors put their checkbooks back into their Patagonia vest pockets and turn their attention to their portfolio companies as everyone tried to figure out how to navigate a pandemic.

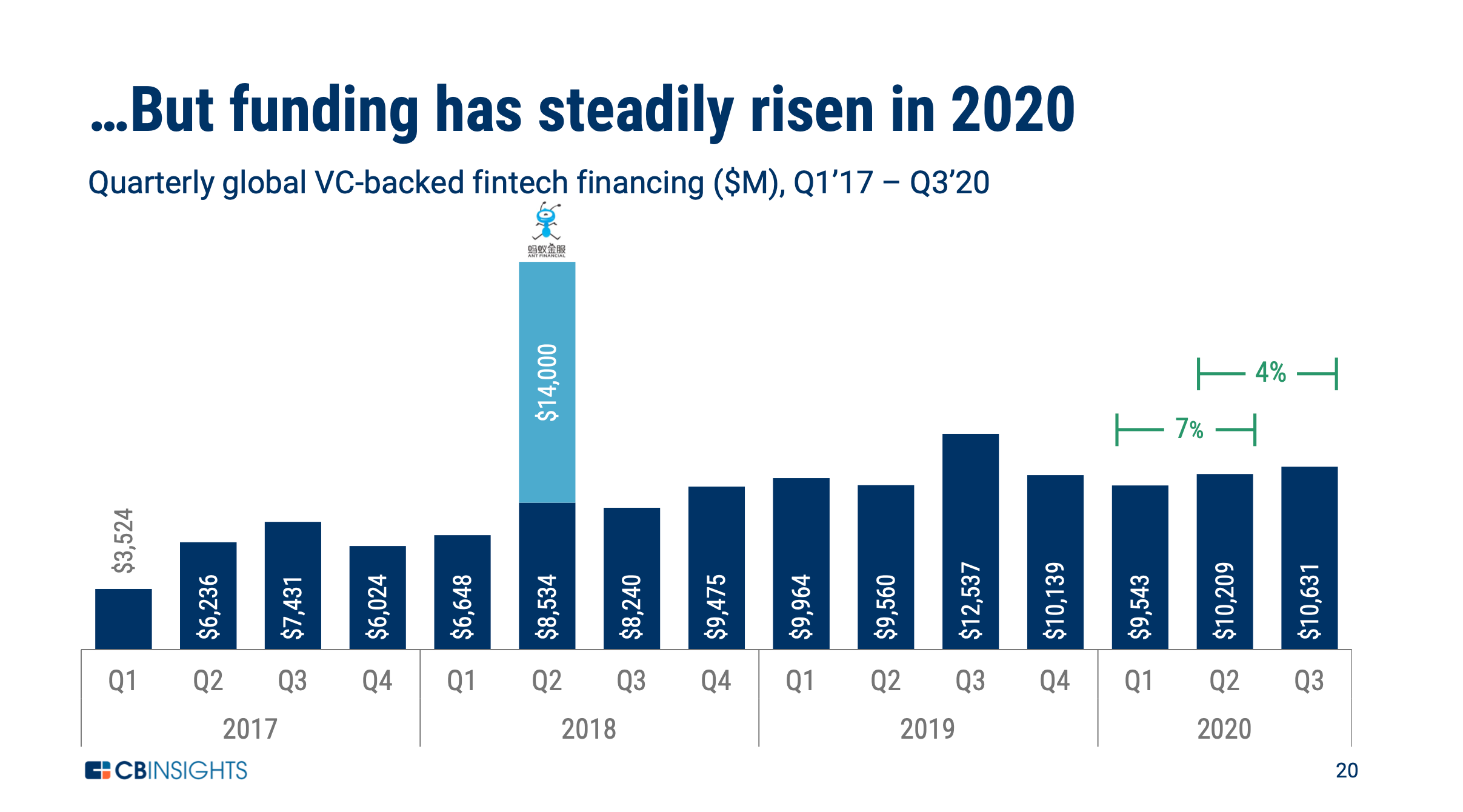

The first quarter of 2020 quickly fizzled, with funding falling off a cliff. However, in March, the market regained momentum. In Q2, we saw a modest uptick in deal volumes and overall funding compared to Q1 (it was up 7% over Q1 in dollars invested). As I noted in my Q2 roundup, the agile VCs (who weren’t already doing so) quickly adapted to taking pitches over Zoom, and we saw investors pop their heads back up with their checkbooks in hand.

Meanwhile, many FSIs were caught flat-footed in their ability to adapt to the changing landscape. For some, it became abundantly clear that being fully digital needed to move from “it’s on our 2-5 year transformation roadmap” to being implemented yesterday. This was exacerbated by government stimulus packages globally relying on banks as critical intermediaries. In many countries, this exposed how far behind legacy FSIs were on the digital adoption curve as compared to fintechs.

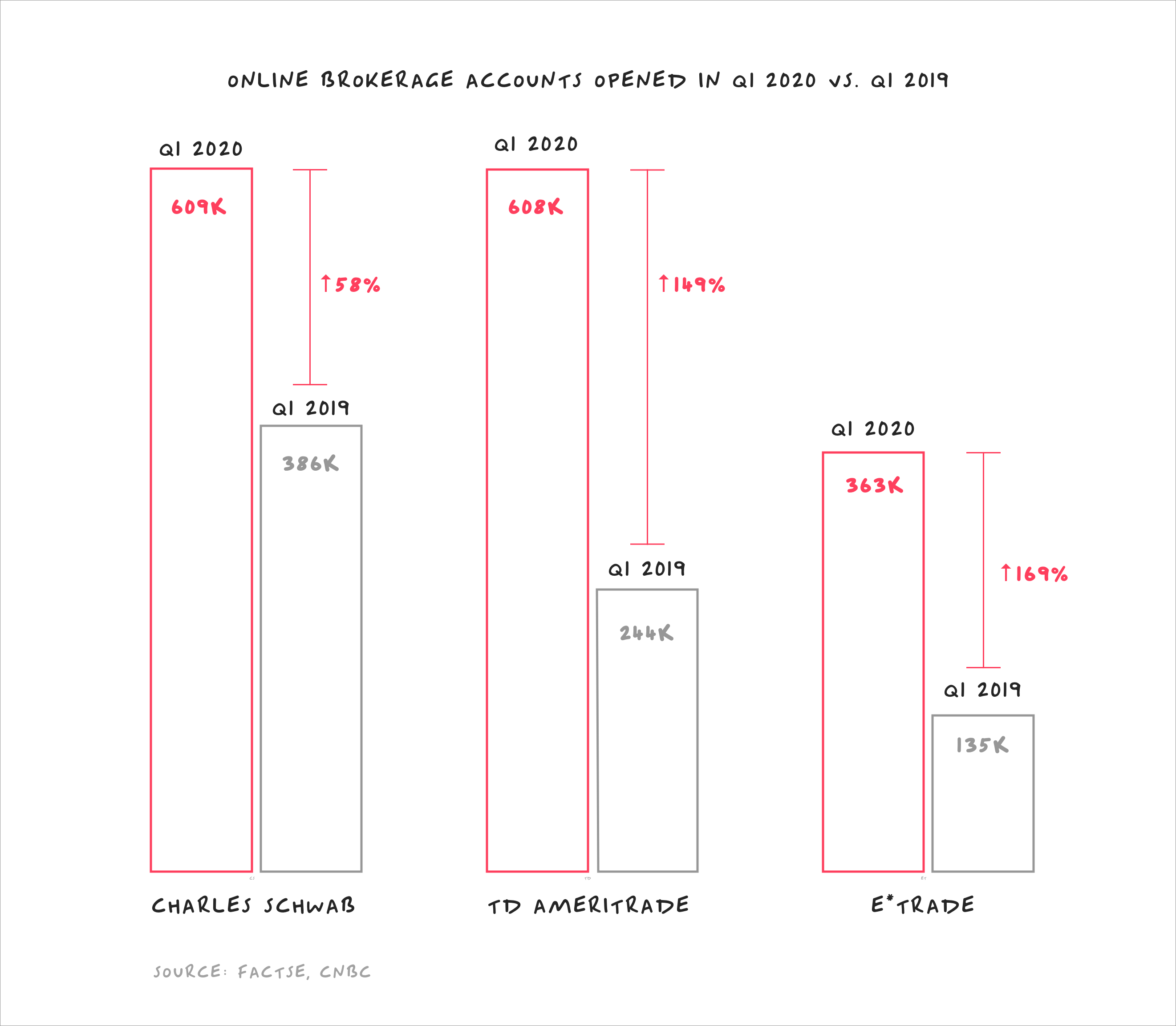

Meanwhile, on the consumer fintech side, the first half of the year saw various trends that had been developing start to accelerate as consumers looked to take advantage of a digitally native solution. For example, there was a meaningful increase globally in the adoption of contactless payments as people avoided cash and a sharp rise in e-commerce penetration. As capital markets surged, we also saw people open in droves online brokerage accounts - which not only benefitted Robinhood but also many of the listed brokerage shops too.

At the close of Q2, fintech was back to its frothy self, deals were humming along, and investors in private markets were riding high on the momentum we saw in the broader public markets.

🔥 Mega Deals Continued To Dominate And Angels Investors Returned

Just as we saw in Q2, investors reached into their kegs of dry powder and loaded up some big shots during the quarter. A large portion of this dry powder was deployed into later-stage companies, with 60% of all funding for the quarter being pushed into mega-rounds ($100m+ rounds of funding). Some notable funding rounds included:

Robinhood’s $660m Series G;

Klarna’s $650m growth round;

Bright Health’s $500m Series E; and

Chime’s $485m Series F.

Overall, this resulted in a slight increase in the dollars deployed in Q3 (up 7% over Q2). However, as noted above, the capital deployed was heavily skewed towards more mature companies - meaning that if you removed the mega-round financings, overall dollars invested were actually down by 16%. This was also reflected in the number of deals completed, which fell for the fourth consecutive quarter.

Although this might be cause for concern, it does reflect the fact that the industry is starting to produce some mature companies that are emerging as category leaders. A great example of this is the BNPL space which is starting to consolidate with more acquisition activity by the AKAs (Afterpay, Klarna, Affirm). For example, Afterpay acquired Pagantis in August for $82m and Klarna bought Moneymour and Spring Marketplace earlier this year.

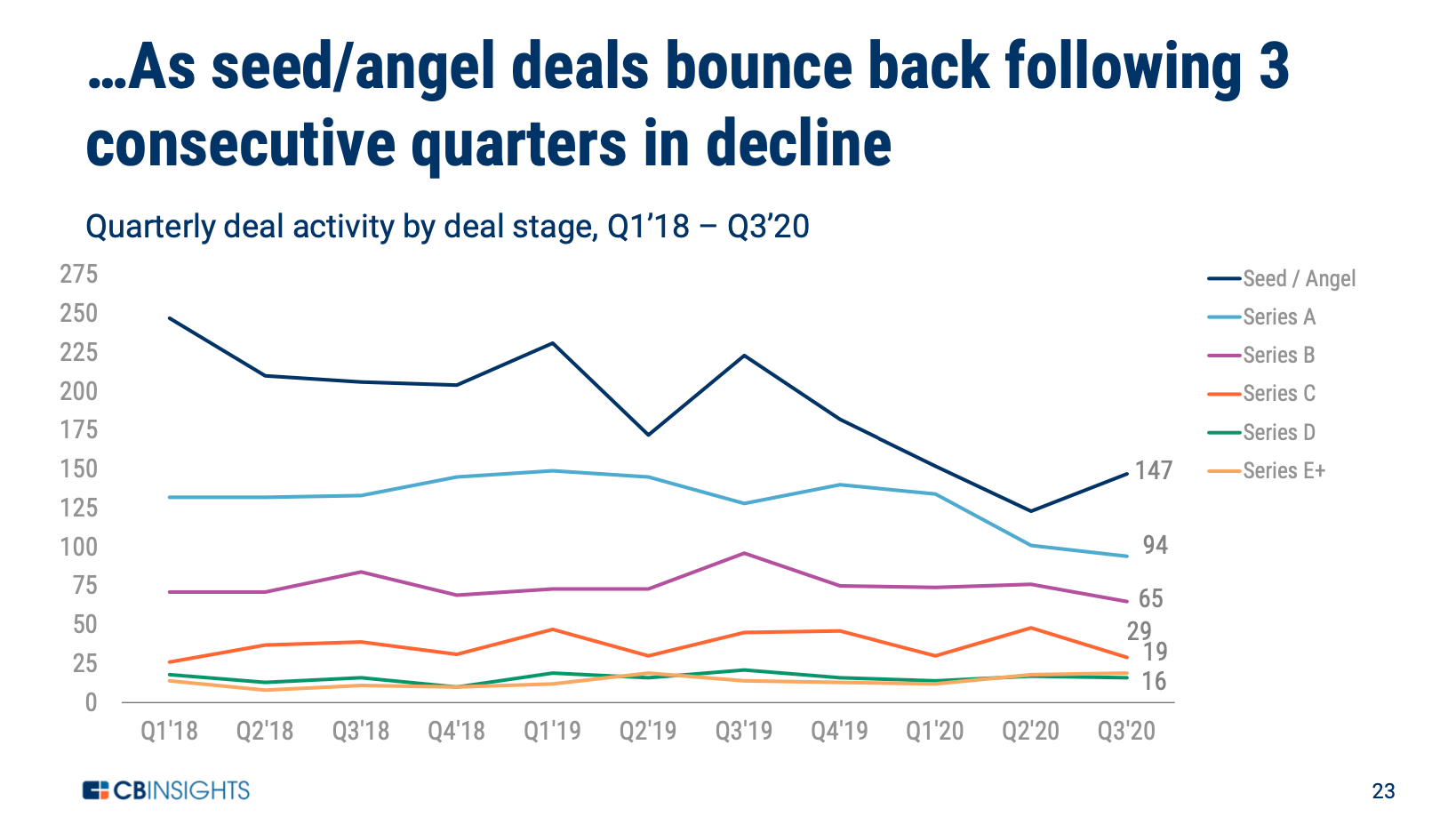

Interestingly, Q3 also saw an increase in the number of seed/angel deals completed. Overall, early-stage deals were up by 20% from the previous quarter, which is the first time in three quarters that deal volume has increased for this stage of funding. In part, this reflects the heat we’re seeing in early-stage deals - especially for those companies playing in the financial infrastructure space. Along with this, the growing international attention fintech is receiving and the opening of opportunities in markets like Africa and South America resulted in seed-stage deals being up.

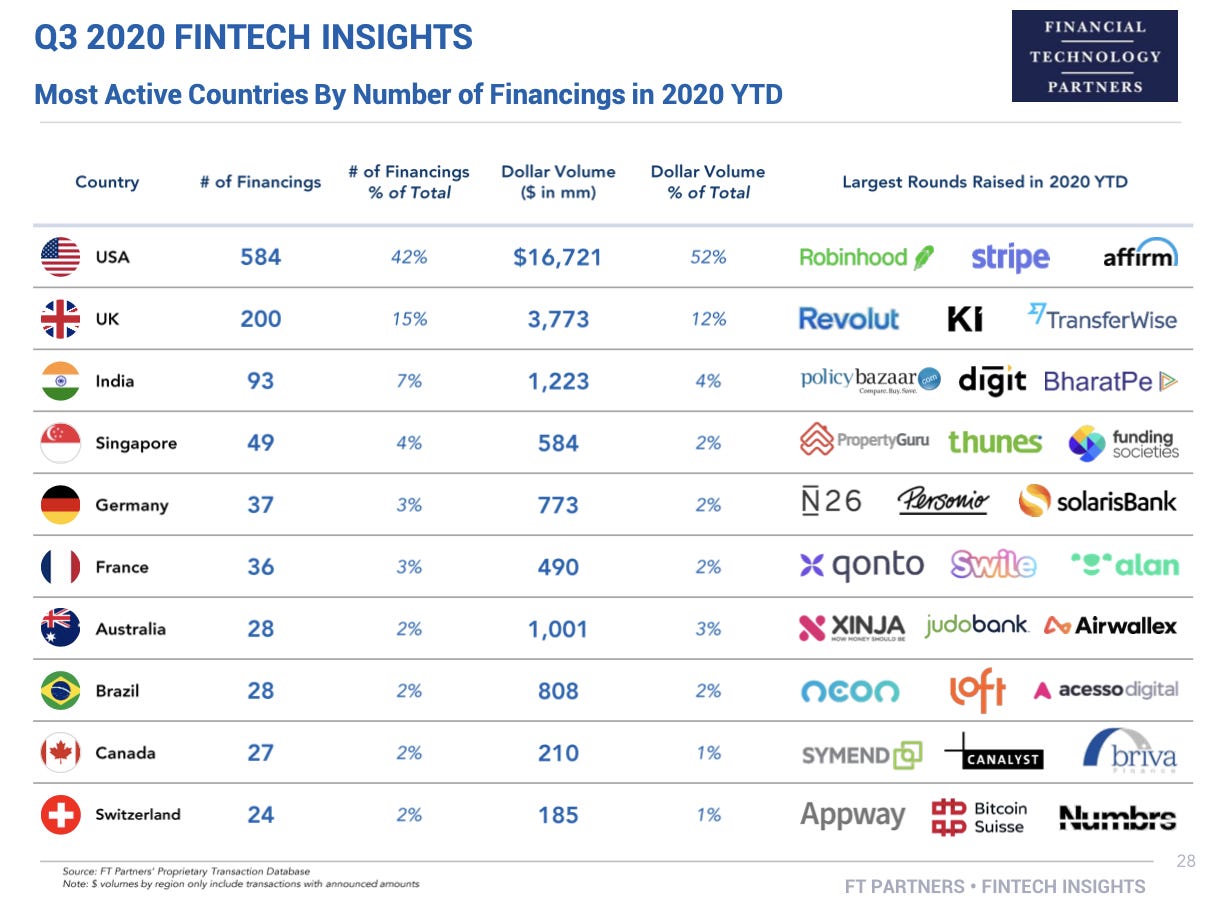

Geographically, as you might expect, the most active country in terms of deals completed was the US. Having said this, Europe and South America were the only regions to have shown quarter over quarter increases in the number of deals completed and total funding. It’s also worth noting that Africa and South America were the only regions that saw deal volumes increase for every quarter in 2020.

🥡 Takeaway: The rich got richer in this quarter. Money being pumped into fintech darlings was emblematic of the broader mega-round trend we’ve seen this year, as investors continued to pile in behind the category leaders. It’ll be interesting to see if this continues in Q4 as a number of the capital hungry fintech unicorns hinted that they might go public late this year/early next year. A trend I think we’ll see continue is the rise in seed/angel dollars flowing into fintech. It’ll be driven by continued growth in operator funds, the rise of rolling funds, and the renaissance in angel investing by the beneficiaries of windfall gains coming from public market listings.

📈 The IPO Market Continued To Run Hot

This year has been a bumper year for IPOs in fintech with 22 listings globally this year, 15 of which occurred in Q3. Unsurprisingly, the bulk of companies elected to list on US ticker (17 of the 22 listings were in the US).

The only thing hotter than a traditional listing this year has been a special purpose acquisition company (SPAC) listing. Fintech was not immune to SPAC-mania, with a bunch of fintech-focused vehicles hitting the market. These included:

FinTech Acquisition III’s merger with Atlanta-based payment processor Paya;

FG New America Acquisition Corp raising $225M led by Joe Moglia;

FTAC Olympus Acquisitions raising $750M led by Betsy Cohen;

Gores Holdings IV’s merger with United Wholesale Mortgage; and

FinTech Acquisition Corp. IV priced $200M.

Also worth mentioning in the context of listings, is the recent clampdown by competition regulators on tech companies and their growing interest in fintech. The most notable being the case brought by the DOJ regarding Visa’s acquisition of Plaid. Although, the matter is just kicking off the impact is likely already being felt across corp dev teams at incumbent FSIs. It’ll be interesting to see the effect it has on Q4 M&A activity and whether this will be the impetus some companies need to pursue going public.

🥡 Takeaway: As equity markets pump and the demand for fintech stocks continues to climb, we’re likely to see investment bankers courting fintech startups in a push to take them public. Some big-name fintechs are waiting in the wings and have already indicated they could be ready for their stage call in late 2020/early 2021. These include Robinhood, Marqeta, AvidExchnage, and Flywire, to name just a few - so get ready for more fintech listing activity at the end of the year.

🏗️ “Plaid, but for…”

The “Plaid but for X” search went into hyperdrive in the second half of the year and continued into Q3 as investors clamoured for their piece of the fintech infrastructure pie. This meant that some of the hottest deals in Q3 were B2B fintech infrastructure companies. Interestingly, these deals ranged from early-stage financing in companies like Moov and Alloy to later-stage fintechs like Flywire. Irrespective of the stage they invested in, every VC was converted to the religion of “everything is fintech.”

Although, from the outside, it might feel like investing in financial infrastructure has been the quickest trend to go from thesis to meme - the reality is that there is still a lot of work to be done in modernising the way companies interface with the legancy financial rails. As a quick reminder, 95% of ATM transactions touch a COBOL code base, and the world can’t keep relying on the COBOL Cowboys to save the day every time there is a major system outage at a bank. To be fair, this is unlikely to change anytime soon, but modernisation will occur if not for the simple fact that fintechs are the ones who are adopting a more modular banking stack.

🥡 Takeaway: There is still a ton of heat in the fintech infrastructure space. This is mainly being driven by the big underlying trend that more companies are looking to integrate financial services into their products and would rather use modern plumbing to connect to the copper pipes that are the legacy financial rails. However, as with all trends, it’s also becoming a massive magnet for the tourist investors looking for the next Plaid. I think things will cool off a little as the tourist dissipate and the fintech faithful stay, but are more discerning in the way they deploy money into the segment.

🔮 Predictions For Q4

Before we jump into my Q4 predictions, I thought I’d quickly reflect on how I did with my Q3 naval gazing.

Things I got right:

My prediction that more angel/operator fund money would come into the sector was fairly spot-on.

The continued interest in infrastructure was also on point. To be fair, this wasn’t that out there as a prediction.

More money being poured into unicorns was also correct - but again, not all that controversial.

Things I got wrong:

Challenger banks continued to expand internationally and there weren’t any clear signals that they’d tired of getting shellacked in their expansion jurisdictions.

No banks went ham and spent big dollars to acquire a fintech for >$1bn. Unfortunately, Dj-DSol didn’t decide to go on a spending spree (and luckily didn’t end up slicing off a piece of Marcus for Axe)

Ok, now for some Q4 crystal balling.

We’ll see some degree of pull back in the embedded fintech space as investors try to figure out where the real (vs imaginary) hot spots are. Tied to this, I think the narrative around embedded payments will calm down as early adopters of embedded fintech product focus more on the low hanging fruit - like simple insurance products and embedded lending.

I think we’ll see interest return to SMB lending as a new wave of players enter the market trying to solve the working capital needs of companies (à la Square Capital). I don’t think this meaningfully plays out in Q4, but feel like it’s a trend we’re likely to see gain further momentum as a result of embedded lending products getting more popular.

The end of the year will bring with it a rush to IPO for some fintechs. The large number of SPACs who are ready to begin their “unicorn mating dance” will also drive more activity. I’d keep an eye on some of the slightly ‘mustier’ fintech unicorns, who might be tempted to SPAC it up.

Coming back to embedded fintech, I think there will be more interest in the benefits management space as it becomes clearer that it is a natural distribution point for embedded offerings - for example, see Gusto wallet.

At the end of Q4, I’ll circle back and again do a review of my predictions. Until then, have a great Q4 (or what’s left of it), and may all your investments become unicorns 🦄

📖 References

The data used in this piece was organically harvested from the following reports:

CBInsights: The State Of Fintech Q3'20 Report: Investment Sector Trends To Watch

FT Partners Quarterly FinTech Insights and Annual Almanac - Q3 2020

🙏 What did you think of this week's issue of FR?

I love it! ◌ I Like It ◌ Not Bad ◌ I Don’t Like It ◌It’s Awful