Issue #7: Robinhood Gets The Bag, Euro Challenger Banks Struggle In The US And It's Time To Understand Moats

Issue #7: Robinhood Gets The Bag, Euro Challenger Banks Struggle In The US And It's Time To Understand Moats

👋Hi, FR fam. I hope everyone has had a great week and is keeping safe.

Fintech doesn't sleep and this week is no different. Let's jump straight into it and begin with Robinhood's $280m series F raise.

🏹 Wanna r/wallstreetbets?

Without a doubt, one of the funniest corners of finance on the interwebs is the 1.2m strong subreddit r/wallstreetbets. For the uninitiated, they describe themselves as 4chan meets a Bloomberg Terminal - which probably gives you a sense of the shenanigans that happen on this subreddit. It's the place to go for stock trading memes and bragging about getting the bag after purchasing put options that are close to expiration - just like this guy did.

When you click into the numerous Yolo trade threads, you'll notice one consistent theme - Robinhood. The weapon of choice for these 'swipe and tap' traders isn't TD Ameritrade or Charles Schwab; it's a startup that launched in 2013.

Robinhood, the no-fee trading app, has been a viral hit from the day it launched. Most in startup land will have seen (or even copied) the now famous Robinhood referral system - the one that landed them 1 million preregistrations for the app. In many ways, it seems they have captured the zeitgeist of a generation who are looking for ways to engage with brands they know and love all while trying to make bank.

Robinhood has been hitting the much sought after millennial market hard. The average age of a Robinhood user is 32, and users check the app on average ten times per day. With these kinds of numbers, along with the size of the market, it's no surprise they've been able to raise a $280m series F at an $8.3bn valuation.

Their monster raise comes on the back of a surprising uptick in new customers (they've added 3m new customers this year) as stock markets go wild during COVID-19 and the challenges associated with a surge in users (they had an untimely outage during on the busiest trading days in the app's history).

However, it hasn't been all clear sailing for the startup. Robinhood has been facing increased competition from the old guard of brokers who are also following suit and offering free trading. In fact, Charles Schwab, TD Ameritrade, E-Trade, and Fidelity all offer commission-free trading now. This combined with the inevitable question of how they make money in the long run when the average account size is $1,000 - $5,000 seems to pose a real question around how they grow from here.

Part of the answer to this question is from Robinhood Gold (their premium subscription service) and Payment for Order Flow (PFoF), but the real long-term play has to come from offering other financial services products - it almost feels inevitable now that they’ll become a full line bank. Taking a leaf from the SoFi playbook, it’s clear that Robinhood’s success will be determined by what other products outside of trading they end up offering their customers. So look out r/wallstreet, you might soon be graduating to r/homeloans.

💰 Notable Funding Announcements

I feel like I say this every week, but I'll say it again, it's been a big week for raises in fintech land. This week, $1bn was raised by fintech startups across 34 deals globally, showing just how hot the sector still is.

🥋Judo Bank this week announced a fresh round of funding. The Australian based SME challenger bank raised a whopping $230m from their existing shareholders, who include Bain Capital. According to reports, the valuation is 'well over' a billion, which places the SME challenger bank in rare air here Australia, as only the second privately held fintech unicorn.

🤓My Take: As I've said in previous issues, the SME banking segment in Australia is ripe for disruption and is very much up for grabs as the big 4 Australian banks continue to drop the ball on this highly profitable market. The more interesting question is, what will the winner in this space look like? My guess is they won't merely be offering an incrementally better customer service experience as compared to the big 4 Australian banks but a new way to bank online. It’ll be interesting to see whether Judo Bank is the one that’ll figure this out.

🇩🇪 German challenger bank, N26, announced a $100m top-up to their series D round of financing this week. According to reports, their valuation remains at the series D valuation fo $3.5bn.

🤓My Take: N26 has had a mixed year, with the announcement a few months ago that they’d be shutting down operation in the UK due to Brexit - which probably pointed to the fact they'd been struggling against Revolut, Monzo, and Starling to get cut through in the comparative UK market. Having said this, their US expansion seems to be tracking well, with 250,000 users signing up their product as of January 2020. Further, Brazil, a market N26 has signaled that they're targeting could prove to be an exciting growth lever for them - Nubank has proved there is a real desire for alternatives in this underserved market.

🐕 Bought by Many, the UK pet insurance company that has in total raised £120m in funding, this week announced that they'd raised an additional £78m in capital. The company currently insures more than 200,000 pets across the UK and Sweden.

🤓My Take: In the stale world of pet insurance, Bought by Many is really mixing it up and providing an interesting playbook on how to market a niche financial services product. For example:

They offer insurance coverage for exotic pets - which has by in large been an area ignored by incumbents. However, it’s where you'll find some of the most passionate pet parents who are more than happy to talk about products they love to other pet owners.

Also, by offering insurance to pet businesses - like dog walkers - they’ve activated another passionate base of pet influencers who help them spread the word about the company.

📧 Feel free to flick me an email if you have any exciting news you'd like me to share with the FR community. I'm me@alantsen.com and @alantsen on the Twitters.

Ps. If you like what I'm doing with FR please feel free to share it on your social disinformation network of choice. Also, I'd appreciate it if you forwarded this newsletter to a friend you think might enjoy it.

📰 News

🏃♂️Moving FaaSt — The Finance-as-a-Service TechScape

This is less news than an interesting take on the Finance-as-a-Service landscape. As the piece notes, one area that's is commonly under-discussed in the world of fintech is the finance/treasury function in a company. If you've ever used products like Concur, Gusto, or ADP, you know precisely what I'm talking about.

I totally agree that there is a bunch of white space and room for improvement in the finance/treasury stack of companies. Having said this, these are some of the most entrenched products in a company, and very few have found a GTM that works. The fact is, Karen in payroll doesn't want to learn how to use a new product - and no one wants to get Karen angry. However, with just the public companies in this space worth $200bn+, it's space worth well worth knowing more about and one I try to keep an eye on.

🇱🇹 Revolut launches licensed bank in Lithuania.

UK challenger bank, Revolut, officially launched as a licensed bank in Lithuania this week. Along with the announcement of the launch, they also revealed that they currently have 300,000 customer accounts in Lithuania - which is a staggering number. This means that roughly 10% of the country has a Revolut account.

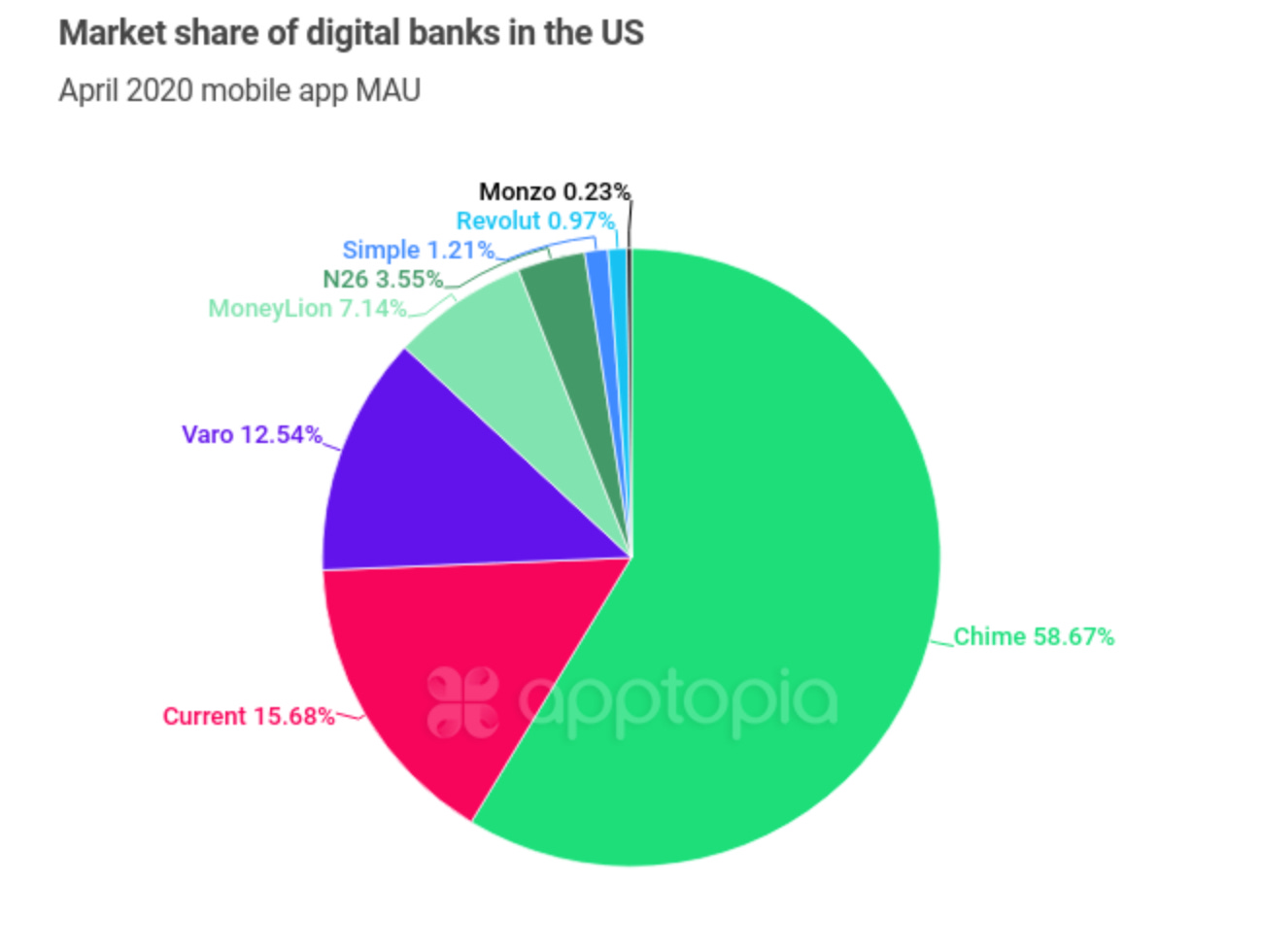

🇺🇸Europe's digital banks off to slow start in the US market

Sifted pulled some fascinating data from Apptopia that suggests that the European challenger banks are having a hard time of it in the US. Specifically, it shows the big two UK challengers (Monzo and Revolut) have just a 1% market share of the challenger bank market based on monthly active user (MAU) data. This is as compared to Chime, Varo, and Current, who hold a little over 70% of the market.

To be fair, it's still early days for the European challenger banks in the US - most haven't even been in the market for 12 months. So it might be too early to tell how it shakes out. Having said this, most haven't ventured outside of the EU (where they can take advantage of passporting of licenses), and those who have are struggling to gain traction.

I think the US will be an interesting battleground that will prove out if challenger banking is a global or regional game. My guess is that in 24 months most of the UK challengers will head back across the pond with little to show for the adventure.

🏦 Banking the rich and famous: the rise of private digital banks

This piece highlights an area of fintech I'm fascinated with - hyper verticalised banking. Although I've never heard of the startup they mention in the article, the idea that private banking could be available to a tier lower than the $10m minimum required by Goldman Sachs feels inevitable.

As the cost of BaaS continues to fall it’s likely that the SME banking space will also see more verticalised propositions - watch out for tradie bank.

🥶 From Cold Storage

Potentially, two of the most abused words in fintech startup pitches are 'platform' and 'moat.' If you listen to enough pitches, you’ll learn that apparently every startup is a platform and has a defensible moat.

To help turn the tide on the abuse of these innocent words, I thought I'd include a piece this week from Jerry Neumann on moats. In it, he lays out the different types of moats that exist and their relative strengths and weaknesses.

For example, this is how he describes GS's know-how moat:

The continuing success of Goldman Sachs in the highly competitive investment banking industry is due in part to collective tacit knowledge passed from senior employees to more junior employees through many hours of supervised work. Some of this knowledge is how to do the work itself–this then becomes individual tacit knowledge–but some of it is how to effectively work with each other and within the firm. This knowledge is only useful if others within the same firm have complementary knowledge. Even if star individual performers or whole teams are hired away, only a part of the collective tacit knowledge moves with them, rendering it much less useful.

Special know-how is a weak moat for startups.

Trust me, it’s well worth a read.