Issue #35: What People Get Wrong About BNPL, The Rebirth Of Google Pay And Affirm Drops Their S-1

Issue #35: What People Get Wrong About BNPL, The Rebirth Of Google Pay And Affirm Drops Their S-1

👋 Hi, FR fam. I hope you’ve all had a great start to the week.

It seems this week has quickly become Buy Now Pay Later (BNPL) week in fintech circles. In the US, we saw Affirm drop their S-1; meanwhile, the Aussie corporate law regulator released their report into the BNPL sector.

To make sure FR isn’t left behind, I also thought I’d pen some thoughts on the sector and what I think most people get wrong about it.

What Most People Get Wrong About BNPL

If you were to summarise most news coverage of the BNPL sector, it would basically round to “it’s making kids buy more stuff they don’t need and driving them into debt.” More specifically, the coverage usually invokes the tone of a worried parent warning you of the perils of easy debt, drugs, sex, and rock’n’roll. Ok, maybe not the drugs, sex, and rock’n’roll stuff, but definitely the debt bit.

However, this is far from the truth. In fact, the data suggests something else is sitting behind the meteoric rise of the BNPL sector.

Australia has been the epicenter of the BNPL industry. In fact, the ASX is home to some of the largest BNPL companies globally, and cumulatively the 7 listed entities are worth close to $35bn AUD — with Afterpay accounting for much of that.

A recent report by the Australian Securities and Investments Commission (ASIC) sheds some light on just how big the sector has become in Australia. Here is a quick snapshot of the industry.

It’s worth pointing out that the sector grew 5x in terms of customers in just 2 years, and the number of merchants using a BNPL facility has increased by 45x for ZipPay and 50x for Afterpay. That’s some extraordinary growth.

So what’s driving the uptick in the use of BNPL?

According to the same ASIC report, it’s actually a lot less sinister than the easy credit narrative most would have you believe. In fact, the report notes that:

90% of users believed that buy now pay later arrangements allowed them to ‘manage spending by spreading payments over time’

More interestingly, most people tied repayments to a debit card or transaction account (74%) even though more than half had credit cards (51%). Further, 74% reported never missing a repayment, while the percentage of BNPL transactions that incurred a missed payment fee was only around 14% as of June 2018.

Although it’s a much more boring story, the data suggests that BNPL is a way Millenials and increasingly Gen-Z manage their money. If a credit card’s “job to be done” is the deferral of payment when you have the money, BNPL has basically done that in a more digitally native and convenient way.

As much as banks can’t wrap their heads around the fact that credit cards are dying, they are, and no amount of rebranding will change that. It’s much more conducive to clicks to say the industry is endangering the financial health of Gen-Z, but the real story here is how some Aussie companies (and a Swedish one too) disrupted the credit card industry by reinventing layaway payments.

📣 The News In Brief

The Clevland Cavs now have their own credit card. The first LGBT+ focused challenger bank launches. Built For Mars drop their final installment in their series on the UX behind PoS terminals. Chase becomes the latest bank to dive into BNPL. Paypal is still the biggest game in town when it comes to unsecured business lending. Uber and Marqeta cozy up. Gemini enters the UK with a little help from Clearbank. Starling looks to kick off the Bannister Effect when it comes to challenger banks becoming profitable. Douugh hits the US. Thoughts on vertical banking, how fintech helped during COVID, the calculus behind payments and QR codes going mainstream from the team over at A16Z.

📈 Notable Funding Announcements

Fundraising numbers were up this week, with fintech companies globally raising a total of $864m across 43 deals.

🏓 Paddle Raises $68m In A Series C Funding Round →

Last week, software billing startup Paddle announced that they’d closed a $68m series C funding round that was led by FTV capital. The round also had participation from existing investors, including Kindred, Notion, and 83 North.

🤓 My Take: For some readers of FR, your initial response to this might be “who?” For some context, Paddle describes themselves as a “revenue delivery platform” — marketing speak for we do payments and some other value-added stuff like sales tax compliance and subscription management. As you might imagine, this feature set is geared towards SaaS businesses.

According to the announcement, they’re currently serving 2,000 clients across 245 countries and have seen “…average annual revenue growth of over 175% over the last four years and doubling in the last year alone”. Impressive.

Companies like Paddle show there is still a bunch of whitespace in online payments — the world isn’t dominated by Stripe (yet?). There are likely several sizable businesses still to be built that offer services on top of the checkout experience. One need only look at the feature releases of many larger gateway providers to see that “value add” is where things are at.

🛍️ Juni Raises A £2m Seed Round →

E-commerce focused challenger bank, Juni, announced their £2m seed round. The round was led by Cherry Ventures and had participation from some high profile angel investors.

🤓 My Take: The SME challenger bank space continues to run hot globally, with a new one seemingly launching every month.

What’s interesting about Juni is its focus on e-commerce. More broadly, the verticalised challenger bank model is gaining more momentum. The highly focused approach makes a lot of sense — if you can find a group that can be clearly defined and you can offer them a differentiated product that addresses their needs, this can be a great ‘land’ strategy — with the ‘expand’ essentially being the age-old banking strategy of cross-selling.

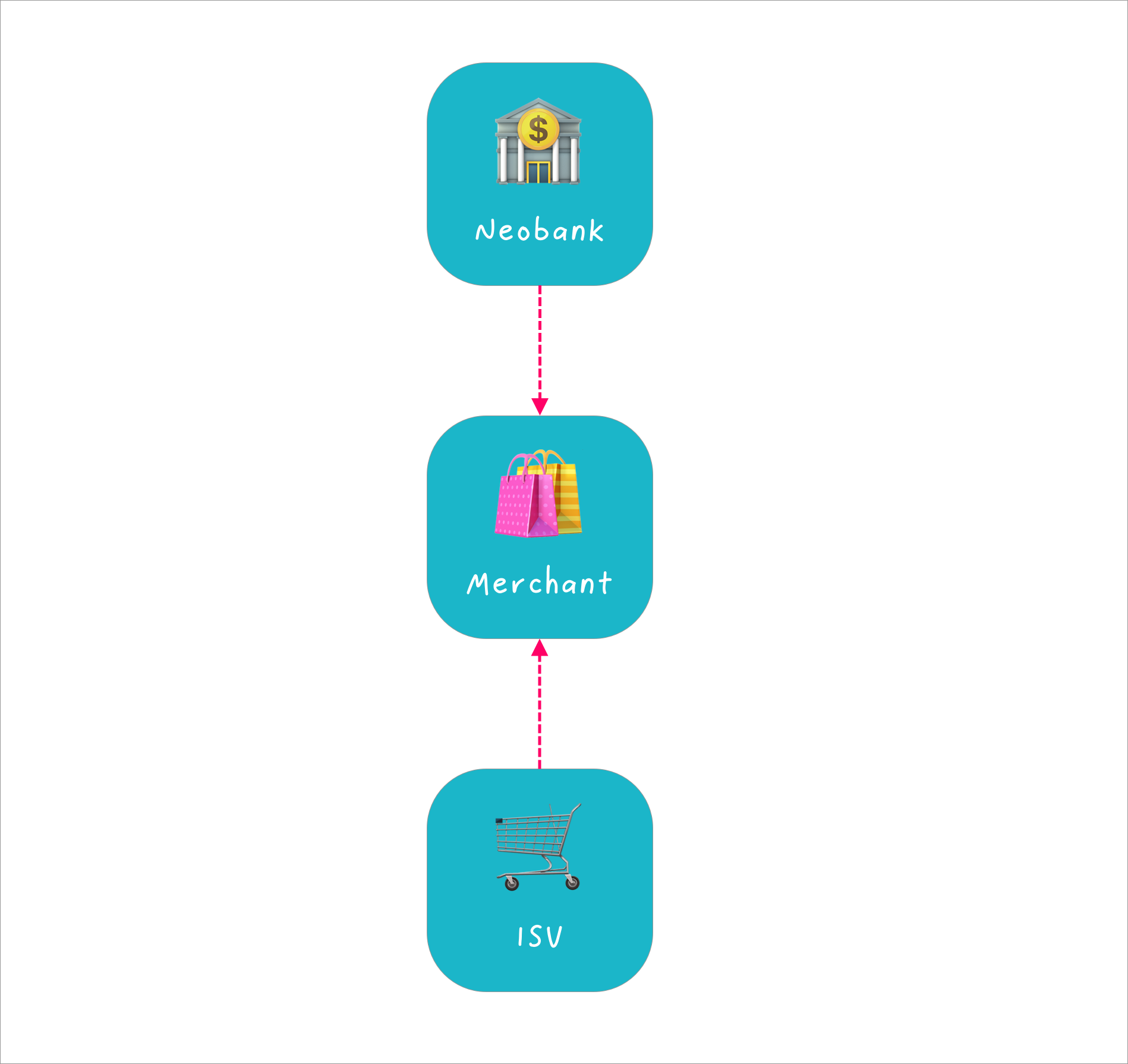

One of the more interesting questions here is, who is best positioned to offer banking service to e-commerce players? Is it a hyper-focused neobank, or is it the upstream ISV (in the e-comm space that would obviously be Shopify) that offers its sellers financial services products?

It’s still an open question, but with the increasing number of embedded fintech offerings, the embedded ISV solution is looking more likely to come out on top.

🏗️ Griffin and Modulr Raise Seed Rounds →

Griffin and Modulr both announced capital raise this week.

Paypal Ventures led Griffin’s £9m round, and EQT Ventures anchored modular’s £6.5m round.

🤓 My Take: It feels like every week I beat the fintech infrastructure drum here at FR. Having said this, it’s hot for a reason. The demand for fintech infrastructure services continues to grow as every company becomes/wants to become a fintech.

In Griffin's case, they provide a BaaS solution for fintechs and established brands looking to venture into FS. While Modulr provides a platform for companies to manage and automate the movement of payment flows and counts Revolut as a customer.

It’s interesting to see the slow changing of the guard in the fintech infrastructure space. We’re starting to see many of the companies who initially provided financial plumbing to the first wave of fintech (I2C, GPS, et al) challenged by upstarts looking to overtake them. The battle is heating up in every market, and it’s definitely a segment I’ll continue to beat the drum about.

☝️ Things You Should Read About

This week Google launched a massive redesign of Google Pay and revealed its banking partnership expansion with a new product called Plex.

Let’s start with the redesign of Google Pay. Basically, they’re rolling out a three-tab setup that reflects the core way consumers interact with their bank account. The “Pay” tab will allow you to make peer-to-peer payments and look at your transaction history; “Explore” will be where you’ll find deals and discounts; and “Insights,” which is designed to aggregate your financial history and provide you with insights.

Another way to say this is that they’ve mashed together Venmo, Honey, and Mint in one product.

To be clear, that’s not meant to be a dig at the product. In many ways providing all of that on a single platform should be a powerful thing — especially if you’re the main way people interact with payments daily (i.e., Google Pay). If you take that one step further and combine it with Andriod as your distribution channel, it could be an amazing way to back your way into being the home for a person’s financial life.

The other thing they announced was Plex, which is a new banking service where they intend to offer partner banking accounts. According to reports, they’ve lined up 11 banks and credit unions as partners. When setting up a new account, the customer will be able to choose who they go with. At launch, they’ve started with Citi and Stanford Federal Credit Union.

Again, in theory, this could be a power move for Google. The ability to intermediate a banking relationship and be the interface into a customer’s daily financial life could make them the central hub for all banking relationships.

However, the challenge for Google has never been product. This might be controversial, but I actually think they generally build solid fintech products. By in large, their products are thoughtfully designed and function exceptionally well. Instead, the issue for Google has been a commitment to the FS business. Their usual MO is that they launch a very on-trend product to some fanfare and then, 24 months later, walk it out to the back paddock and unceremoniously put it out of its misery.

For example, here is a sample of FS products they’ve scuttled in the past once they lost interest:

BebaPay (2013-2015)

Google Checkout (2006-2013)

Google Wallet Card (2013-2016)

Google Hands-Free (20016-2017)

I hope this time is different. However, I don’t think it takes a clairvoyant to predict that we’re likely to see another fintech product added to the Google Graveyard in 24 months.

🥡 Takeaway: Google has tried numerous times to get serious about financial services. However, the challenge seems to be to keep that momentum going. This time might be different for Google, with the tailwind from success in other markets (most notably India) hopefully showing them that this can be a meaningful business for Google.

Happy BNPL week!

As mentioned, above it seems like everyone is writing about BNPL this week, with most of the chatter being instigated by Affirm’s S-1 dropping.

Let’s start with some of the headline numbers.

For context, this puts them a fair bit behind Aussie BNPL juggernaut Afterpay who have 9.9m customers, 55,400 merchants, and did $11.1b in GMV for the FY2020 financial year.

One thing that many were surprised by was the high concentration of their revenue in one customer. According to the filling, Peloton accounts for a staggering 28% of its revenue for the fiscal year 2020 — which is about ~$142m. Now that’s a lot of Peloton bikes! In some ways, this might not be surprising given the sticker price on a Pelton bike, but many were surprised that the VC indoor bike of choice was this large a piece of the revenue pie.

Notably, Affrim also revealed that they’ve been improving their net loss position. In the current quarter, losses fell by about 50% from a year ago — to $15.3 million. The biggest uplift in the costs came from increased sales and marketing, where expenses rose due to their new partnership with Shopify.

🥡 Takeaway: BNPL continues to be a hot segment in fintech, and Affirm is riding the wave masterfully. The listing’s timing is bang on, as the US market is just starting to show signs of interest in this payment method.

💳 Mastercard Gets The Regulatory Greenlight To Acquire Finicity →

Not sure that this necessarily surprised anyone, but Mastercard had their acquisition of Finicity greenlit by the DOJ. Congrats Mastercard and Finicity!

Meanwhile, Visa has been battling it out with the DOJ over their acquisition of Plaid. Although one might put it down to the fact that there isn’t a smoking volcano in this acquisition, it’s probably to do with the fact that Finicity is more of a pureplay data aggregator that, on the surface, doesn’t seem to have any payment initiation ambitions.

Having said this, I think many would find it hard to imagine that Mastercard bought Finicity purely to get into the data aggregations space — but now that the acquisition has received regulatory approval, I suppose we’ll never know.

🥡 Takeaway: Visa has fallen into a regulatory quagmire, and what once looked like an astute acquisition could turn into a headache. On the other hand, Mastercard seems to have got out cleanly while making a similar land grab. It’ll be interesting to see how this impacts Visa and Mastercard as they survey the fintech landscape for their next acquisitions.

🎧 Podcast Recommendations

Another week, another set of recommendations for your listening enjoyment.

Banking Can't Ignore The GenZ Potential → This one is from a few weeks back now, but I thought I’d drop it in this week as it’s a great chaser for all the discussion around BNPL in this issue of FR. This pod is an interesting listen and covers a bunch of research into Gen-Z’s attitude towards money and their relationship with incumbent FSIs.

Yoni Assia on eToro’s Incredible Growth →Yoni Assia is the founder and CEO of eToro. This is a great listen and it was fascinating to hear the story behind the company amongst other market-related topics like SPACs, the rise of the millennial investor, and even sustainable meat. Well worth a listen.

❤️ Show Some Love For FR

📈 You can check out Radar, an open database of Australia's fintech ecosystem. You can find it here → 📡 SideFund Radar

📧 Feel free to reach out if you want to connect. I'm me@alantsen.com and @alantsen on the Twitters.

📸 As always, our cover image is provided by Death To Stock Photos. You should get your stock images from them too.

Ps. If you like what I'm doing with FR, please feel free to share it on your social disinformation network of choice. I'd also appreciate it if you forwarded this newsletter to a friend you think might enjoy it.

🙏 What did you think of this week's issue of FR?

I love it! ◌ I Like It ◌ Not Bad ◌ I Don’t Like It ◌It’s Awful