Issue #32: Embedded Fintech In All The Right Places, GS Makes Moves Into BaaS, And Shopify Partners With TikTok On Social Commerce

Issue #32: Embedded Fintech In All The Right Places, GS Makes Moves Into BaaS, And Shopify Partners With TikTok On Social Commerce

👋 Hi, FR fam!

Before we dive into this week’s issue, let’s kick things off with some light comic relief. Apologies in advance if this triggers any PTSD for fintech founder 🙏

📣 The News In Brief

Nerdwallet splashes some cash to buy Fundera. Square looks to acquire Credit Karma’s tax preparation business as Inuit tries to avoid potential antitrust issues. SoFi gets one step closer to being a chartered bank. Another banger from Built For Mars, this time, they break down the UX of signing up for a PoS terminal account. A great teardown of Root Insurance’s S-1 filling. Afterpay hits 11.2m global active customers (and almost half are Millenials). Why European fintechs are struggling in the US and what they can do to reverse the trend. Carbon removal meets payments in the crossover no one had on their bingo card for 2020. Monzo and Starling top the charts for switchers. UBS wants to pump $200m into fintech startups. India leads the way in real-time payments, doing an eye-watering 41m transactions per day.

📈 Notable Funding Announcements

It was another big week for fintech fundraising, with companies globally raising a total of $624m across 32 deals.

🚘 DriveWealth Lands $56.7m In Fresh Funding →

Last week DriveWealth announced that they’d closed their Series C round of funding. The brokerage infrastructure player raised $56.7m in a round led by Point72 Ventures. The round also had participation from Raptor Group, SBI, Route 66 Ventures, Mouro Capital and Fidelity.

🤓 My Take:

As retail investing continues to run hot, it feels like every consumer-facing fintech app is trying to incorporate a US equities trading component. Outside of the standalone offering like Robinhood, there’s been a rush by challenger banks to incorporate US equities trading as a feature - which totally makes sense given most are searching for product lines that will drive revenue.

For example, in Australia, Xinja recently announced that they plan to launch a trading app called Dabble, which will let Aussies buy US equities for a flat monthly fee. Meanwhile, we’ve seen Acorns, SoFi, MoneyLion, and Stash all offer equity trading alongside their core product offering in the US. While in the UK, Revolut has been offering brokerage free share trading since 2018.

Much like other parts of the infrastructure stack, most challenger banks have outsourced the actual licensing, custodial, and order execution elements to third parties who deliver the back-end brokerage experience through an API. This has allowed the challenger banks to focus on customer experience instead.

The rise of companies like DriveWealth (who power Hatch, Revolut, Stake, and Moneylion’s US equities trading products) has driven down the technical barriers to entry. Further, when you combine this with the growth in popularity of payment for order flow (PFOF) as the monetisation mechanism (which tends to better align with the challenger bank business model) you have all the requisite elements needed for the rise of embed brokerage offerings.

As one might expect (and as you can probably guess from DriveWealth’s hefty funding round), the companies ‘arming the rebels’ are also doing well from the rising interest in the stock market trading. In the case of DriveWealth, they noted in their fundraising announcement that “…its partners open[ed] more accounts in 2Q than E*Trade, Schwab, and TD Ameritrade combined…”

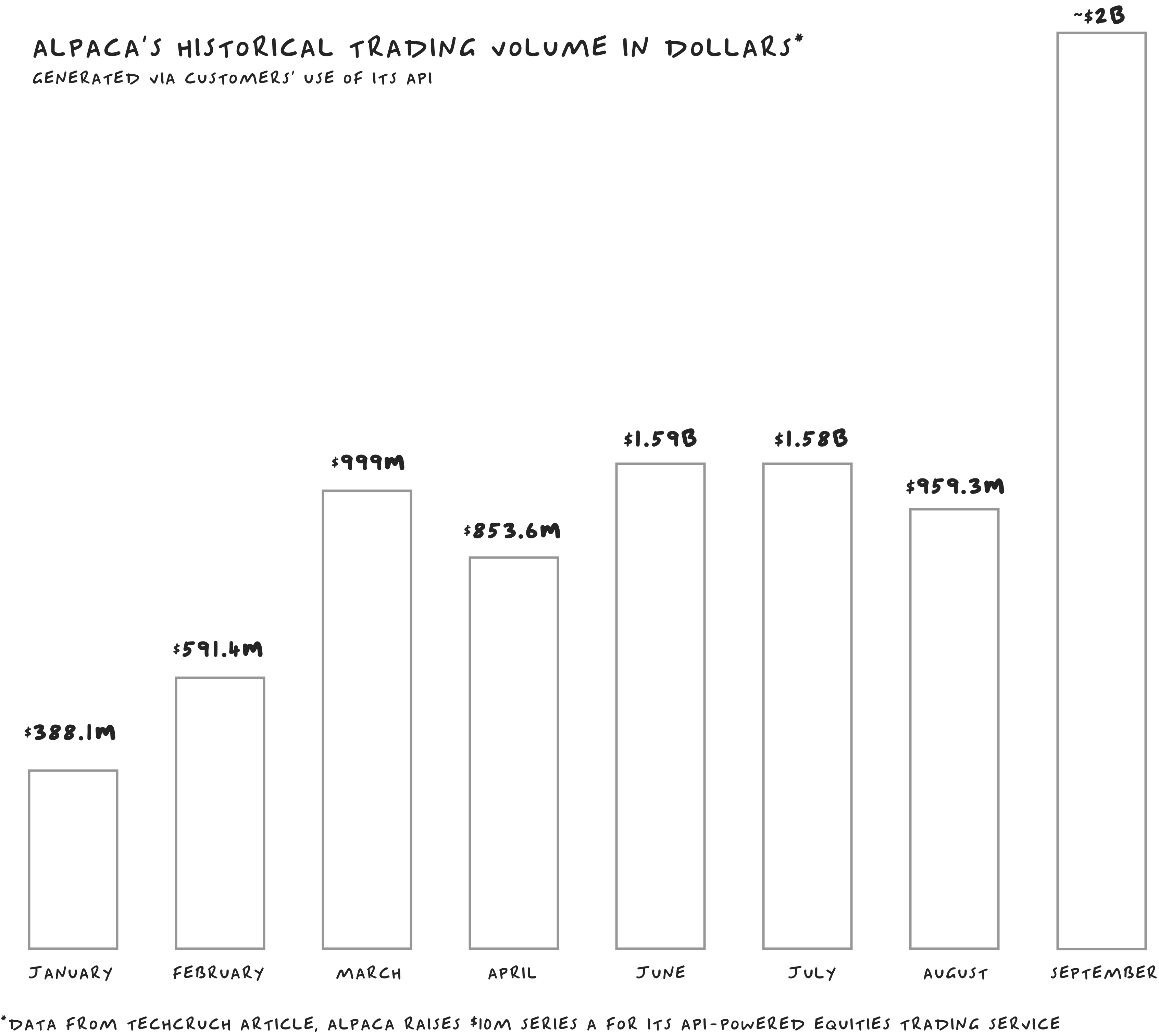

While competitor Alpaca, who recently announced a $10m Series A round of funding, has also seen some healthy growth. According to data disclosed in a recent Techcrunch article, Alpaca has substantially grown their trading volumes. As of September this year, their trading volumes (in dollars) was 10x up on the volumes from the same time last year.

What’s happening in capital markets broadly, and retail investing narrowly has tended to be a good leading indicator for trends in fintech. For example, consumer-centric online trading companies like Trade*Plus and E*Trade and Robo-advisory products were all early indicators of what consumers were looking for in their financial lives - online and better value.

As we move to more embedded offerings, it’ll be interesting to see what other capital markets products become APIs that can be offered in our other banking and non-banking experiences.

🥡 Takeaway: The brokerage business has seen significant changes over the last 4 decades and has always served as a bell-weather for the pace of disintermediation across the whole financial services landscape. As embedded fintech continues its ascent, keeping one eye on brokerage market trends could serve as a good barometer for what could be next for the broader fintech sector.

🦉 Wise Raise $12m To Provide Embedded Finance For Everyone →

Last week BaaS provider Wise announced they’d closed a $12m Series A funding round. E.ventures led the round with participation from Base10 Partners and Techstars.

🤓 My Take:

I’ve noted in previous issues of FR, that I think it’ll likely to be the more mundane FS products that end up being the gateway drug that introduces businesses to the benefits of embedded finance - think, allowing a Shopify store owner to offer extended warranties on headphones (see: Extend) or instant financing for your Peloton (see: Affirm). Which is great and all, but for the most part, not all that exciting. This is why Wise really caught my attention.

In many ways, Wise is the strong form version of what many hope financial services will evolve into - it’ll just appear in the right context, in-line with the ‘job to be done.’ More specifically, Wise allows a company to push the whole banking experience natively into their product. For example, say you operate a two-sided marketplace, using Wise you’d be able to offer bank accounts directly in your product so that sellers on your platforms could hold money, make payments via a bank transfer, a debit card, a virtual card, and also get paid using everything from card payments through to cheques.

For those companies that integrate a product like Wise, they not only have the upside of helping their customer deal with the financial element of their business at the time and place that best aligns with the ‘job to be done’, but they also create a new revenue stream for their business (Wise has a revenue share model on deposits and interchange fees).

🥡 Takeaway: Although most of the initial use cases around embedded finance are fairly mundane, the long term outcome will be that a vast majority of the financial interactions a person has on a daily basis will be done in line with the task that has necessitated them having to interact with the financial world. The companies manifesting this vision are the ones you really need to be keeping an eye on 👀

☝️ Things You Should Read About

🏦 Goldman Sachs Goes Deeper into BaaS →

Goldman Sachs believes developers are creating the future of finance, and to facilitate this, they announced last week that they’re diving deeper into the world of banking-as-a-service.

Opening up the BaaS platform feels like a natural extension to the work they’ve been doing with players like Apple and Amazon. The initial transaction banking APIs will cover payments, treasury automation, and a broader BaaS offering to allow embedded business bank account experiences to be created by third parties.

At their recent investor day, GS hinted at their plans in the BaaS space with some slides that suggest that this really is only the start of their aspirations to build a fully-fledged platform bank.

One of the more interesting elements of the strategy is that GS seems to be starting with the top end of town by offering services like treasury automation. Given GS’ DNA, this totally makes sense and is a great example of a bank leaning in where it authentically has an advantage.

🥡 Takeaway: GS has been on a tear recently, not only with its Marcus product but also with some key partnerships (e.g. with Apple and Amazon). The move into BaaS in a more serious way shows that GS has some huge aspirations in the fintech space. If I were running a Baas startup, I’d be keenly watching what GS is up to as they really are shaping up as a serious player in the space.

🛍️ TikTok Partners With Shopify To Get Into Social Commerce →

The social commerce vertical is heating up in a serious way, and Shopify knows it. As you may recall, Shopify recently minted a deal with Instagram to power their in-feed commerce play, and this week they announced a deal with TikTok. The initial deal will allow Shopify merchants to create, run, and monitor their TikTok ad campaigns directly from their Shopify dashboard. Having said this, the announcement did hint at the fact that they’ll be testing in-app commerce in the future.

To give you a sense of how big the opportunity could be in social commerce for Shopify, it’s worth looking at how large the market has become for this shopping mode in China.

It’s estimated that China's live commerce market for 2019 was worth $63b (an increase of 220% over 2018), with 71% of users watching a live commerce event at least once per week. While on Douyin (TikTok in China), the live e-commerce feature has minted many millionaires using the platform to sell everything from fruit to lipstick. For example, Austin Li (also known as the Taobao ‘Lipstick King) has 45m followers on the platform and netted $145m in sales on Singles Day - which is a hell of a lot of lipstick!

🥡 Takeaway: Shopify is all about ‘arming the rebels.’ The new outpost for many of the rebels is social commerce, so it’s not surprising they’re trying to be the arms dealer of choice. Having said this, social commerce might be the impetus that these platforms need to take their fintech aspirations more seriously.

🎧 Podcast Recommendations

As usual, here are some podcasts for your auditory pleasure.

Frank Rotman - Founding Partner of QED Investors - The Search for Logic → This is a masterclass in fintech investing from one of the best in the business. It’s a must-listen this week.

Building the Digital Financial Infrastructure for Latin America with Ualá → I really enjoyed this great interview with the CEO of Ualá. If you haven’t heard of Ualá, this is a handy little primer on one of the fastest-growing fintech startups in Argentina.

☝️ Lastly, here are some Q3 earnings calls you should definitely listen to → Visa, Mastercard, American Express, Fiserv, Global Payments, and Goldman Sachs.

❤️ Show Some Love For FR

📈 You can check out Radar, an open database of Australia's fintech ecosystem. You can find it here → 📡 SideFund Radar

📧 Feel free to reach out if you want to connect. I'm me@alantsen.com and @alantsen on the Twitters.

📸 As always, our cover image is provided by Death To Stock Photos. You should get your stock images from them too.

Ps. If you like what I'm doing with FR, please feel free to share it on your social disinformation network of choice. I'd also appreciate it if you forwarded this newsletter to a friend you think might enjoy it.

🙏 What did you think of this week's issue of FR?

I love it! ◌ I Like It ◌ Not Bad ◌ I Don’t Like It ◌It’s Awful