Issue #31: Afterpay To Offer Savings Accounts, Benefits Management Platforms As The Next Embedded Fintech Vertical And JP Morgan Wants To Take Square On

Issue #31: Afterpay To Offer Savings Accounts, Benefits Management Platforms As The Next Embedded Fintech Vertical And JP Morgan Wants To Take Square On

👋 Hi, FR peeps. I hope you’re all living your best life this week!

Let’s get this week’s FR started with a little ditty from Colin, who’s upset about his local Barclays branch closing (H/T: Chris Glenhill). Although old mate isn’t going to with a Grammy for this performance, it’s super cute. It’s also a great musical reminder that not everyone is excited about banking going fully digital.

📣 The News In Brief

Don’t count Visa or Mastercard out just yet. The ugly side of the US’ KYC-AML obsession. Paypal dives deep into crypto. The great rebundling in fintech continues. The FDIC released some fresh data on how Americans bank. The new Monzo premium card costs a whooping £50 to produce. Yandex pulls the pin on its acquisition of Tinkoff Bank. Lufax, the Chinese lending company you’ve probably never heard of, is embarking on a $2.4b US IPO. Mastercard invested in Marqeta two weeks ago, and last week, Visa dropped money into GPS as the card-issuance and processing space continues to run hot. The Australian Competition and Consumer Commission (ACCC) are concerned about Australian banks buying fintechs - even though the major banks haven’t made a significant acquisition in the last 24 months 🤷♂️

📈 Notable Funding Announcements

It was another big week for fintech fundraises, with companies globally raising a total of $1.8b across 30 deals.

🏥 Bind Benefits Raises $105m →

Bind Benefits last week announced that they’d closed $105m in fresh capital. The Series B funding round was led by Ascension Ventures.

🤓 My Take: When looking at the benefits management space, there are so many nooks and crannies one can fall into. Part of the reason for this is how broad the term has become in the modern organisation. For many companies, this has come to refer to everything from medical coverage and contributory pension schemes (e.g. superannuation, 401K) right through to specific benefits a company might offer - like an L&D stipend.

The structure of the US healthcare systems ends up meaning that in amongst managing L&D and commuter benefits, medical insurance ends up being a critically important part of benefits management. To put this in perspective, ~50% of Americans obtain their healthcare coverage through their employer-sponsored health benefits plan. From an operating perspective, when you combine this with the fact that coverage cost has been rising exponentially over the last decade, it ends up meaning that for the average US employer, healthcare can often be the second-largest operating expense after wages.

In the micro to SME space, this has opened up the opportunity for companies like Zenefits, Gusto, and Rippling to come in and offer tooling to manage the complexity associated with running a benefits program while monetising on the combination of a SaaS model and a clip of the ticket on insurance premiums. The commission from insurance carriers can be between 2% and 10% - which is a meaningful number when annual premiums can be $20,000 per employee.

Meanwhile, from the mid-market to the larger end of town, the rising costs associated with healthcare coverage have resulted in more and more employers choosing to self insure their employee health plans. In fact, over the period 1999 - 2017, the number of employers with more than 200 employees going down this route increased from 60% to 79%. In the case of Bind, they started out administering health plans for self-insured employers. Specifically, they offer a self-funded administration service (ASO) platform for larger employers like Best Buys, who is a customer. The company is now moving into the fully insured health plan market for SMEs with 50 employees or more on the books.

Interestingly, to date, we’ve only seen Gusto through their wallet product, leveraging their installed customer base and offering embedded finance products. With more modern players stepping into the ASO administration space to act as TPAs, it’s highly likely we’ll see more platforms embedding fintech offerings. These players will likely look to expand the utility of what they’re offering and take advantage of the large customer base they can access at effectively $0 CAC.

🥡 Takeaway: We’ll likely see more embedded finance offerings in the benefits management space as these platforms look to leverage their large installed base to offer products that align with improving their user’s financial wellness. In many ways, this is a perfect place for fintech offerings to be distributed. These customers are already financially engaged with the core product (and therefore already have some degree of trust in your platform) and the extension into products like savings accounts feels like a natural addition to the offering.

Newfront Insurance Raises $100m →

Insurtech startup, Newfront last week announced that they had raised north of $100m since their launch from investors, including Founders Fund and Meritech Capital. As part of the announcement, they also noted that their most recent funding round valued them at $500m.

🤓 My Take: If you’ve ever purchased business insurance, you’ll know firsthand how unpleasant the experience can be. As with most insurance types, purchasing coverage is confusing, time-consuming, and way more complex than it should be. To be fair, part of the reason is that every business is unique, and trying to parse the different offerings a company needs does require a certain amount of skill and time.

Historically, this has meant that SME owners have turned to brokers to determine what policies should be taken out and to bundle them up into a package that best suits the business. However, this experience has generally not been a stellar one for SME owners. This is reflected in the average net promoter score for brokerages being abysmally low - which sits at a fairly poor 17 in the US.

As you might expect, this has meant that SME owners have turned to direct channels (specifically online) to purchase coverage. For example, as you can see from the graph below, the use of brokers in Australia for SME insurance has been on the decline for quite a while, which is also happening in most other markets.

The continued disintermediation of the broker channel has resulted in more prime insurers moving to direct channels to sell SME insurance offerings. However, as noted above, part of the challenge in the corporate insurance segment is that most businesses are unique. To some extent, there is a need for judgment when determining the right coverage - for example, imagine being Uber or Airbnb trying to determine the appropriate insurance coverage required for their businesses when they launched. For this reason, brokers still play an important role in the choices of coverage, as you can see from the data below.

What’s interesting about Newfront is that they’ve very much gone against the grain by trying to empower brokers with modern tooling vs. trying to remove them from the picture. As they note in their press release announcing their raise, brokers can be a valuable asset in advising clients:

Gordon and I launched Newfront in 2017, a year in which several startups were attracting huge investments with a goal of eliminating insurance brokers. We were convinced that their approach was dead wrong. We had already spent countless hours with CFOs, GCs, risk managers, and business owners and concluded that skilled insurance brokers are a foundational requirement for high-quality risk mitigation. The problem wasn’t the broker, it was the brokerage. The typical brokerage forced brokers to behave like data collection and paperwork processing machines, preventing them from deepening their skills or providing expert advice.

To date, the approach seems to be working for them, with their business growing 12x over the last two years and 3.5x in the last year.

In many ways, Newfront seems like the antithesis of what investors look for in the insurtech space - the business relies on brokers and is empowering them to do their job better vs. removing their role from the insurance purchasing process. This approach is very reminiscent of what Atrium was trying to do in the legal space. It’ll be interesting to see how this approach pans out.

🥡 Takeaway: In insurtech much time is spent thinking about how to remove brokers from the picture, it’ll be interesting to see if modern brokerages like Newfront can crack the nut on empowering experts to augment the ‘machines’ vs disintermediation them. Models like this are worth keeping an eye on as they point to a model that might blend the best of both worlds - humans and tech.

☝️ Things You Should Read About

🛒 Afterpay To Offer Savings Accounts Through Westpac →

Afterpay last week announced that they’re partnering with Westpac to launch savings accounts and cash flow tools in Australia. The products will sit on Westpac’s BaaS offering, which is powered by 10x Future Technologies. This will make Afterpay the first fintech to take advantage of Westpac’s BaaS platform.

Shortly after announcing the deal, Westpac announced that they’d be selling their holdings in Zip - which will likely net them ~$366m at the closing price on the day of the announcement.

According to their announcement to the market, the savings product Afterpay will be offering will operate as a fully-fledged savings account:

Afterpay customers will be able to use their new savings account to conduct the majority of their money management activities, including paying bills, withdrawing cash and budgeting. Further services and tools will be introduced over time to drive even more benefits to customers

Afterpay moving up the stack and offering a chequing account makes a ton of sense. In fact, the only thing surprising about it is that it took this long to happen. If you look abroad, Klarna has held a banking license in its home country of Sweden since 2017.

Moving from a monoline business is an important move for Afterpay and signals their intent to be the centre of a consumer’s financial life. This may seem obvious, but the way they’re executing it in Australia (via a BaaS provider) sets them up well for the US - where they’ll inevitably need to partner with the likes of a Green Dot to launch a savings card offering Stateside.

Afterpay is an absolute beast of a company, and this is another signal that they might have started as a BNPL company, but that will likely prove to only be their first act.

🥡 Takeaway: There is no doubt that consumer savings accounts are just the start of Afterpay’s journey to become a multi-line FSI. What is commonly under-discussed with Afterpay is how they’ve been able to straddle both consumer and business customers - serving them a product they both love. I assume they’ve started with consumer banking to build their decisioning models further, but I could see them quickly moving into the world of business banking, which would be a real game-changer for the company.

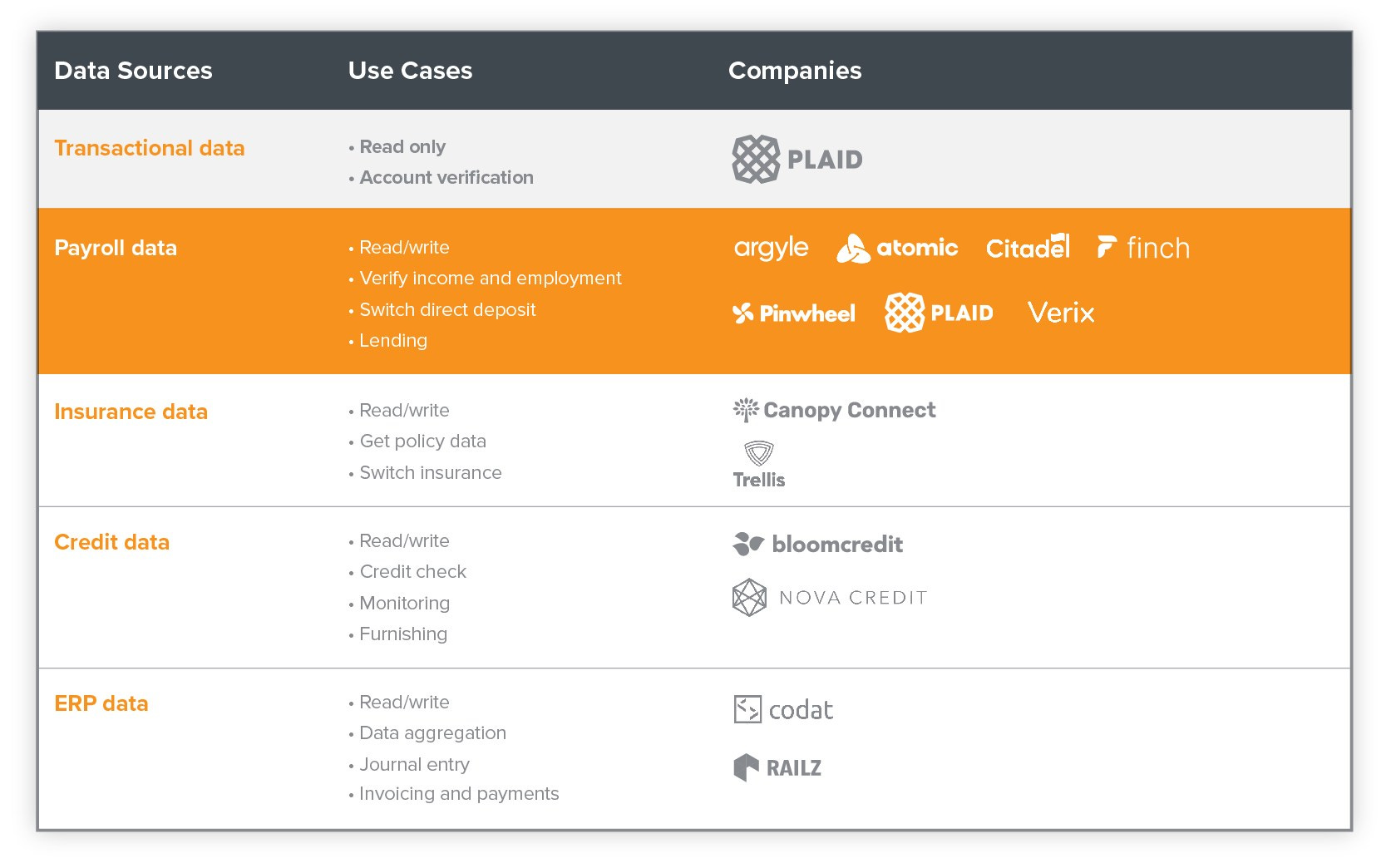

💰 The Promise of Payroll APIs →

This is another great piece from the A16Z team and well worth a read.

As I discussed last week, the unbundling of the pipes that come in and out of banks is well underway. As this article discusses, a ton of value can be unlocked when you look at how the data that travels through these pipes can be unlocked and used in new ways.

🥡 Takeaway: The ‘headless’ fintech segment continues to get hotter, with new ‘pipes’ being unlocked regularly by B2B fintechs. However, what is emerging is a need to orchestrate all these different sources of information. As much as there is a focus on the raw data, there is a growing interest in the middleware that’ll help bring this all together.

Last week JP Morgan announced the launch of QuickAccept, a service that allows businesses to take card payments through either a mobile app or a contactless card reader. The product is aimed at the lower end of the market, with JP Morgan aiming it at businesses with less than $500,000 in annual revenue. According to Jen Roberts, CEO of the Chase business banking unit, they’ll migrate “a large portion” of their 3m business customers onto the new product.

The really interesting part of the announcement is that JP Morgan will be offering ‘fast funding’ for free (which is usually charged for by the likes of Square). In a world where card readers have basically become a commodity item that is basically free, it’s interesting that moving money more quickly is what JP Morgan is focusing in on as the differentiator.

It’ll be interesting to see if it makes a dent in the meteoritic rise of Square - I’d be guessing it won’t.

🥡 Takeaway: It’s always good to see incumbents having a crack at a market that was disrupted 10 years ago. I’ve read some articles noting this could be an interesting challenge to Square. The reality is that many have dabbled in the PoS space since Square revolutionised the segment over a decade ago, and no one (including Amazon) has been able to displace them as the fastest-growing company in the vertical. I doubt JP Morgan will be the one to do it.

🎧 Podcast Recommendations

Don’t worry all you podcastoholic, I got you covered with three pods you can load up for you next run 👊

Plaid's John Pitts on the Current Regulatory Landscape, COVID FinTech Adoption, and More → This is a short sharp pod on the current open banking landscape in the US. Well worth a listen if you’re interested in learning about s1033 of the Dodd-Frank Act.

Open Banking two years on - how far have we come? → This is an open question at the moment for many countries that have adopted a regulatory-driven approach to Open Banking. This is a solid pod that covers the UK and EU experience and well worth a listen.

WeBank: The Most Advanced Digital Bank in the World → WeBank is a fascinating Chinese challenger bank. This pod is an excellent primer on their operations and how they operate in the hypercompetitive Chinese market. Well worth a listen if you haven’t heard of them.

❤️ Show Some Love For FR

📈 You can check out Radar, an open database of Australia's fintech ecosystem. You can find it here → 📡 SideFund Radar

📧 Feel free to reach out if you want to connect. I'm me@alantsen.com and @alantsen on the Twitters.

📸 As always, our cover image is provided by Death To Stock Photos. You should get your stock images from them too.

Ps. If you like what I'm doing with FR, please feel free to share it on your social disinformation network of choice. I'd also appreciate it if you forwarded this newsletter to a friend you think might enjoy it.

🙏 What did you think of this week's issue of FR?

I love it! ◌ I Like It ◌ Not Bad ◌ I Don’t Like It ◌It’s Awful