Issue #29: Headless Fintech, Why Every Company Wants To Take SWIFT On And Some Podcast Recommendations You'll Thank Me For

Issue #29: Headless Fintech, Why Every Company Wants To Take SWIFT On And Some Podcast Recommendations You'll Thank Me For

👋 Hi, FR fam. I hope you’ve all had a great start to the week.

Let’s get into it this week with a quick chaser to last week’s mention of Step using TikTok influencers to launch their product.

This is one of the posts from Addison Raee, another TikTok celebrity. Not sure what you think, but I don’t think this hit the way they expected it would.

📣 The News In Brief

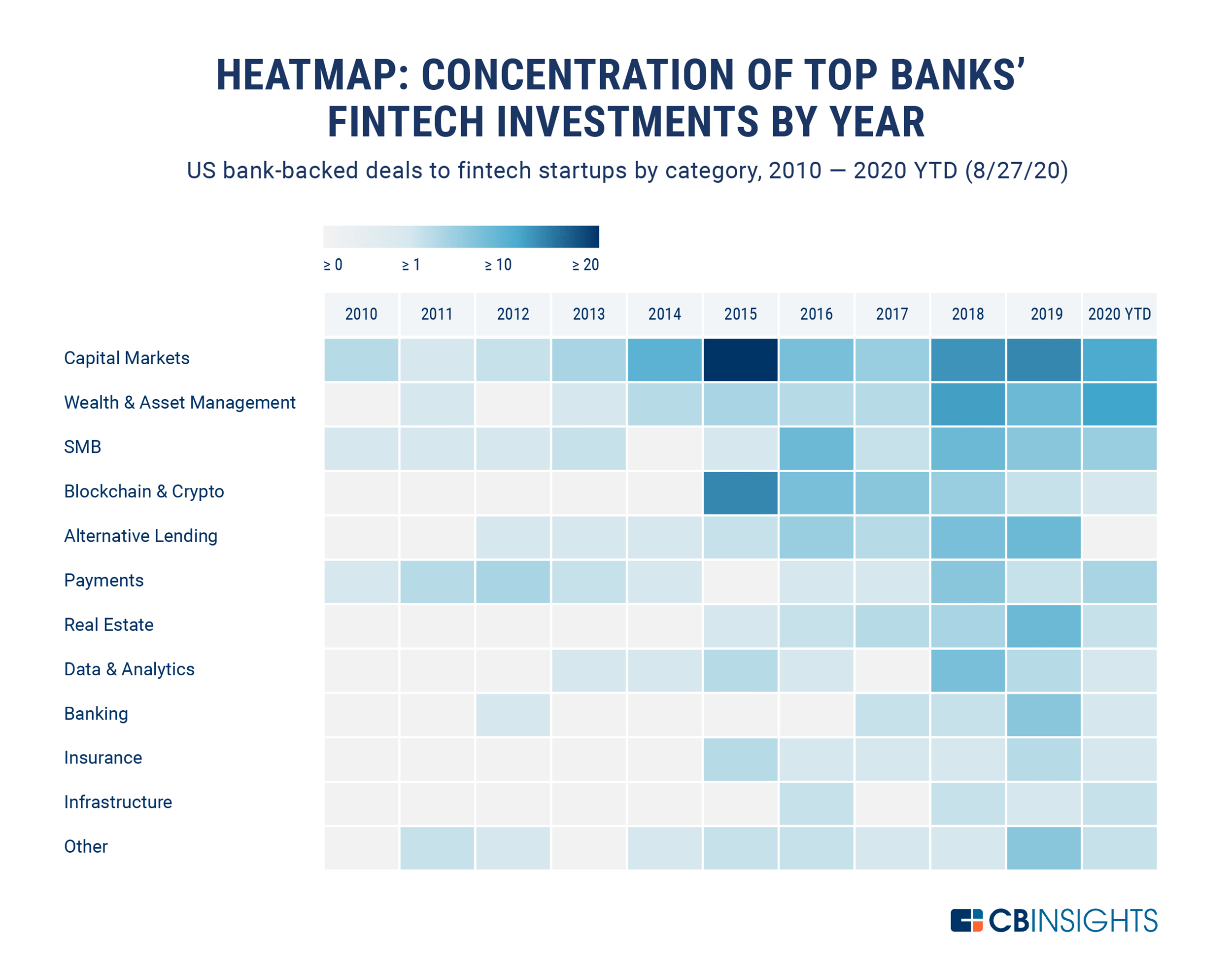

Revolut gets serious about the US. Affirm is looking to go public soon. Square bets big on bitcoin, and Jack shares how they did it. Who’s running Monzo 2.0? Razor made a card with an LED in it. The incumbent bank reacquisition imperative. More from Mckinsey on payments - and it’s not too bad. Chinese payments providers might not be welcome in the US. Macy’s and Klarna buddy up. Venmo finally launches a credit card. Lastly, where are US banks making bets in fintech?

📈 Notable Funding Announcements

This week fintechs globally raised a total of $634m across 30 deals.

🌸 Bloomcredit Raises $13m

Last week credit data as a service startup, Bloomcredit, landed $13m in funding. The round was led by Allegis, Resolute Ventures, Slow Ventures and Commerce Ventures who tipped in $10m. The other $3m came in from a previously unannounced angel round which included a host of fintech super angels including Sheel Mohnot and Ron Suber.

🤓 My Take:

Most reader of FR will be familiar with the famous CBInsights unbundling banks image. In the same way, B2C fintechs have been unbundling the front end of banking, ‘headless fintechs’ are doing the same but for every data pipe that comes in and out of an FSI.

{kind=link}

In the case of Bloomcredit, they are providing an API to allow the ‘reading and writing’ of data to the three major national credit bureaus in the US (Equifax, Experian, and TransUnion). You can check out the video below to hear from their CEO about the problem their solving in more detail👇

The astute observer might ask, but what’s stopping companies just connecting directly to the bureaus? I mean, surely they have an easy to use RESTful API? Yeah, well they sort of do, and yes, you could do that for all three bureaus individually. But it’s fairly painful. For example, the data format a company needs to report to the bureaus in (yes, you guessed it) is their own data spec called Metro2 - a standard created by the Consumer Data Industry Association for credit reporting. For a quick glimpse of the spec, check this out. To be honest, I actually pity the backend engineer who has to deal with this. RIP them.

Part of what’s driving the trend of fintech infrastructure players creating these abstractions is that connecting to legacy systems is, well, hard. That may be clear, but the more interesting observation is that companies dealing with these legacy systems are willing to pay (handsomely) to make that experience easier and most importantly, faster. Much like Segment figured out that companies were willing to pay for a single API that allows you to access all your customer data from one place, many fintech middleware players are figuring out that in each vertical FSIs are willing to pay for a better pipe to access or write financial data.

🧾 Nivelo Raises A $2.5m Seed Round

Last week Nivelo announced they’d closed a seed round raise of $2.5m. Barclays and Anthemis and Firstmark led the round.

🤓 My Take:

Managing payments is hard.

When you read that sentence, your mind probably jumped to the challenges associated with accepting payments. You might have even thought about a particular company like Stripe, Paypal or Adyen.

For the most part, when we talk about payments, discussion is usually dominated by really what amounts to discussions about companies who facilitate payments - gateways, merchant acquirers and payment facilitators. However, if you’ve ever interacted with the finance or accounting teams at a company, you know this is just the beginning of what happens when a payment is accepted. In many cases, it can require a combination of accounting for the transaction in another place (or ten), customer service/error rectification, compliance (for some industries) and probably even some software engineering work too.

That’s why we’re seeing more companies start to pop in the payment operations space - a term that’s being popularised by companies like Modern Treasury (whose blog post on the term I highly recommend reading). It simply refers to dealing with the messy nature of handling money in all of the contexts it presents itself in a company.

Payment Ops is not a new field, just as DevOps wasn’t, it’s just that the context for many companies around how they deal with money has changed. Just as many companies have stopped racking their own servers, companies have stopped going to the bank and physically dealing with money. Along with this a better way to deal with how money flows in and out of a company has necessitated better software solutions. Another way to think about it is; who is the CircleCI for payment pipelines? The answer is, it’s usually Julie in accounts. That probably isn’t the best way to deal with how money flows in an org.

In the case of Nivelo, they help companies manage the credit and debit risk on a specific payment rail, ACH. More specifically, they analyse transactions that you pass through their API and then provide a risk score associated with it to help a company identify if it’s a fraudulent transaction or a processing error. Although this might seem niche, ACH caries ~64m wires per day or ~$55t of transaction value per year.

This is a vertical well worth keeping an eye on as we see more companies realise that they’re just as much in the business of moving money as they are in the business of moving packets.

☝️ Things You Should Read About

🧠 The Financial World’s Nervous System Is Being Rewired

This is the first of two articles from the Economist I’m highlighting in this issue, not sure if this speaks to my reading diet this week or whether the Economist is slowly getting more into the fintech space 🤷♂️.

This piece is a really insightful look at the world of international money movement, and the important role SWIFT plays in it. As the article highlights, many companies are trying to displace the Belgin beast that is SWIFT in its role as the master messaging platform for international money movement. Several competitors, like blockchain-based solutions like Ripple, are trying to find a way to route around them. However, the reality is that they aren’t even in the same ballpark when it comes to connectivity to the banking world or carrying the message volumes that SWIFT does.

Regardless, as the piece notes, this dominance has not dissuaded the competitors from trying to take a piece of the pie for two main reasons:

…swift provides all of these. Built over decades, its network is hard to replicate. But most of the world has two incentives to give it a go. The first is political. Although the organisation is not American, Uncle Sam leans on it to pressure friends and isolate foes. In 2018, when America threatened action if it did not exclude Iranian banks, swift quickly complied… [and] The network’s complexity also makes cross-border transfers slow and costly.

It’s interesting also to note that in a time where SWIFT’s dominance is being challenged the biggest existential threat might come from blockchain-based central bank currencies who don’t need to operate on a messaging system.

It’s definitely going to be interesting times ahead for SWIFT… but then again it has been for a long time and somehow they manage to come out on top.

👩💼 The Finance Tech Stack: What is the Current State?

This post from Redpoint is a nice addendum to my above thoughts on Payment Ops but goes much deeper into the belly of the finance function of a company.

Back in the day when I was a junior burger working at a Big-4 accounting firm, one of the many things that shook me when dealing with large listed companies was that basically every part of the finance function was run and communicated through Excel spreadsheets. A major reason for this was that it was the one unifying tool between all the disparate systems a team would need to draw data from.

This is a great piece from the Redpoint team that covers the current issues in the space and specifically the challenges associated with the having disparate systems that don’t integrate (and have never been even thought to be integrated!).

It’s a great read, and I’m looking forward to part 2.

🖥️ How The Digital Surge Will Reshape Finance

This is part deux of the Economist double this week and probably my favourite article from the week.

For all those really online fintech heads who read my newsletter, you probably saw a few people on fintech Twitter post the graph below from the piece.

Although it’s taking a bit of a poetic licence in describing the way fintech and the payments industry is impacting the legacy banking sector, it does highlight how things have changed in the last decade. To be fair banks don't per se care about payment volumes, as it isn’t where they make their money. However, the more important point it conveys (even if it’s using a strange metric to so) is the way consumers are interacting with the financial system is changing, and banks are no longer the sun which everything else in FS revolves around.

The article is a great discussion of how we’re seeing this displacement happen and as you’d expect it wouldn’t be a piece about payments without mentioning embedded payments.

A great read and well worth it for all those needing some new graphs to tweet 😉

🎧 Podcast Recommendations

Here are this week’s recommendations for your listening enjoyment.

OCC Provides Path For Banking Revolution → This is an interview with the Acting Comptroller of the Currency (OCC), Brian Brooks. This conversation is very different from what you might be expecting. Maybe this has something to do with the fact that Brooks is the former chief legal officer at Coinbase.

Kraken Financial CEO David Kinitsky on Crypto's First Bank → As we discussed back in issue #26, Kraken was recently been granted a restricted banking charter in Wyoming (an SPDI). This is an excellent interview with the CEO of Kraken’s new bank entity, David Kinitsky. Well worth a listen to hear what they plan on doing with their license.

❤️ Show Some Love For FR

📈 You can check out Radar, an open database of Australia's fintech ecosystem. You can find it here → 📡 SideFund Radar

📧 Feel free to reach out if you want to connect. I'm me@alantsen.com and @alantsen on the Twitters.

📸 As always, our cover image is provided by Death To Stock Photos. You should get your stock images from them too.

Ps. If you like what I'm doing with FR, please feel free to share it on your social disinformation network of choice. I'd also appreciate it if you forwarded this newsletter to a friend you think might enjoy it.