Issue #21: AmEx Is Looking At Buying Kabbage, Coinbase And Square Are Getting Into Microloans And It's Been A Tough Week For UK Challenger Banks

Issue #21: AmEx Is Looking At Buying Kabbage, Coinbase And Square Are Getting Into Microloans And It's Been A Tough Week For UK Challenger Banks

👋 Hi, FR fam. I hope you’ve all had a great start to the week.

Before we dive into this week’s news, a quick reminder that online payments are still running hot - as is Stripe.

If you enjoy this newsletter, make sure you share it with a friend - remember, sharing is caring!

N26 employees aren’t happy. Facebook is doing something in payments that makes more sense than Libra. Here comes another fintech SPAC. People went wild for virtual Yams this week (yes, this was a crypto thing). BBVA owned SME challenger bank, Holvi, pulls out of the UK after only six months. GM’s credit card business is up for sale, and DJ-DSol’s bank is looking to buy it. Hedge funds are scrabbling as Robinhood stops publishing data about their customers’ trades. Robinhood is also looking to restrict their API. Aussie banks are going to provide data to the Australian Bureau of Statistics - which begs all kinds of questions. Waze is now a fintech. Apparently, card fraud in Australia fell by 19% in 2019 - the most significant decline ever.

This week's fundraising activity was up with 35 transactions, which collectively raised $1.1bn.

AvidXchange this week announced that they’d raised another $119M in funding. This adds to the $933m they’ve already raised.

🤓 My Take: The accounts payable (AP) sector is an interesting one at the moment as companies of all sizes adjust to a WFH world and along with it try to bring their paper-based processes online.

As you can probably guess, this is vertical still dominated by paper and manual processes. In fact, according to a Goldman Sachs report from back in 2018, 70% of B2B payments are paid using paper cheques, and SMEs incur about $2.7t in B2B administrative costs. The market for solutions that automate the process has been around for years and the introduction of e-invoicing is slowly chipping away at this number. However, given only about 40% of companies in the US automate their AP process, there is still a long way to go.

Having said this, the AP space is very crowded with everything from legacy companies like SAP Concur through to more vertically focused companies like Tradeshift trying to help businesses automate their paper-based AP processes.

COVID19 is accelerating the adoption of nearly every area of automation, with AP/AR being an area that companies have been looking at in more detail; not only due to WFH but because of the impact managing both can have on cash flow. As a result, I think we’ll be seeing more investment activity in this space in the coming months.

🥬 AmEx in Advanced Talks to Buy SoftBank-Backed →

This week rumors emerged that AmEx was looking at buying small business lender Kabbage. The deal reportedly would see Kabbage being sold for $850m in an all-cash deal. This would be well below the $1bn valuation they hit after SoftBank invested $250m into them in 2017.

The online SME lending sector has been hit hard by COVID19 with many cutting staff, reducing credit lines and, in several instances, even halting all new origination.

Kabbage hasn’t been immune to the choppy seas over the last few months. During early March, they furloughed staff and suspended customer credit lines as they dealt with the sudden downturn many of its customers were experiencing. In the same month, they started to focus instead on PPP loans and have approved ~200,000 applications and processed more than $6bn in PPP loans.

A little know fact is that AmEx is the biggest provider of SME credit cards in the US - with nearly all of that being to professional service provides like law firms and accountants. So this acquisition would, in theory, sit neatly alongside AmEx’s already large SME credit card business.

This deal comes on the heels of OnDeck’s acquisition by Enova last week for $90m (locally, KKR are looking at buying the Aussie OnDeck business). It’ll be interesting to see who is acquired next in the SME lender firesale.

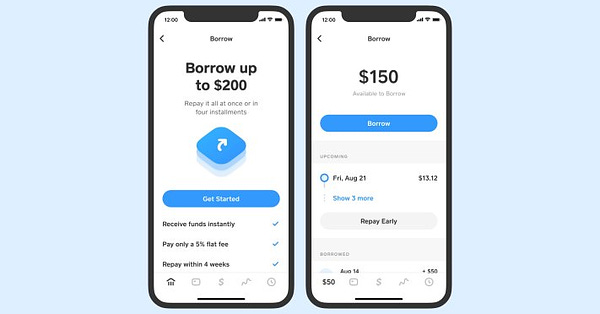

💰Both Square And Coinbase Announce Consumer Lending Products →

Although the Square and Coinbase offerings a quite different, I thought I’d combine them into one news item as they both reflect the embedded lending trend that is emerging amongst direct to consumer fintech startups.

Let’s start with the Square offering. According to reports, Square has been testing a microloan service with around 1,000 customers in its Cash App. Square is starting with unsecured loans between $20-$200. The loan terms are four weeks, and interest is a flat 5% (which equates to an APR of about 60%, which for comparison is lower than the average across the US of 391% 😲)

As the following tweet thread from Maximillian Fredrich of Ark Invest highlights, this looks and feels like the Cash App is stepping into the murky world of payday lending.

To date, we haven’t seen the likes of Chime or Varo try these types of short term loans on for size. However, I think this will change as they all move into lending to bolster their topline revenue. Having said this, with a freshly minted national bank charter Square will have to move carefully through the ethical maze that is payday lending.

Coinbase, on the other hand, is offering bitcoin collateralised loans of up to $20,000. The structure of their loans is again a little different from Square’s, as they are offering an 8% APR with the principle repayable over one year. As they note in their marketing material, this product offering might present a way for those who want to unlock the value of their bitcoin without selling holdings - or for that matter triggering a taxable gain or loss.

To date, most of the big-name neobanks in the US are yet to build a substantial lending business - most seem to still be working through how they authentically offer lending products to their demographic. In the case of Square’s Cash App, this hits right at the heart of their core US demographic (the unbanked who are located in lower-socioeconomic states). It’ll be interesting to see how the like of Varo and Chime approach this space.

🇬🇧Britain's Once-Popular Digital Banks Face A Bruising Reality →

The big 3 UK Challenger banks have had a rough complete of weeks in the media on the back of their annual reports being released.

Monzo, Revolut, and Starling all reported considerable losses and proceeded to get hammered for in the media. However, all showed an increase in customer numbers and revenue over what has been a tough 12 months in the challenger banks sector. Which as you might expect got little air time.

The big outstanding question, especially for Monzo and Revolut, is whether they’ll be able to take the US - which Cash App is showing is much more fertile ground for challenger bank offerings. There is no doubt that global expansion has to be high on the strategic initiatives list for all three, as the small UK market seems to be saturated by challenger bank offerings - which is probably also what their results are reflecting.

This week I’ve pulled out another piece from the A16Z vault. This time it’s on embedded lending - timely read on the back of the news that Square and Coinbase are embedding loans into their products.

Check it out → Fintech’s Second Wave: Lenders in Disguise

📈 You can check out Radar, an open database of Australia's fintech ecosystem. You can find it here → 📡 SideFund Radar

📧 Feel free to flick me an email if you have any exciting news you'd like me to share with the FR community. I'm me@alantsen.com and @alantsen on the Twitters.

Ps. If you like what I'm doing with FR, please feel free to share it on your social disinformation network of choice. Also, I'd appreciate it if you forwarded this newsletter to a friend you think might enjoy it.