Issue #2: Animal Crossing, Vertical Neo Banks And MS Excel Becomes A Fintech Platform.

Issue #2: Animal Crossing, Vertical Neo Banks And MS Excel Becomes A Fintech Platform.

👋 Hi, FR fam. I hope you’re all keeping safe and sane while in iso. I also trust that your sourdough baking skills are levelling up. I know I’ve become bread obsessed over the last few weeks and may have made enough to feed a small French village. I’m worried I might have a bread addiction 😂 Having said this, I’m comforted to know I’m not the only one reading r/sourdough daily.

Now that I’ve got that off my chest, let’s jump into this week’s fintech news.

Everything Is Fintech: New Horizons Edition

Like many other Nintendo Switch owners, I recently buckled to the FOMO and purchased a copy of Animal Crossing: New Horizons. It’s a super wholesome game and is a great antidote to all the craziness at the moment.

While I’ve been busy growing turnips, shopping at Tom Nook’s village store and catching tarantulas more enterprising individuals have been setting up ‘stores’ in the game to sell custom designed in-game items for fiat - using nothing more than WeChat Pay and AliPay QR codes (see the tweet below).

I think this is a super simple (and powerful) example of the ‘everything is fintech’ thesis as it applies to the maker community/passion economy. Specifically, as we continue to see the core building blocks of finance become further atomised (in this case ‘BYO payments’), we’ll see more and more places where people will be able to monetise their skills. More interestingly, in many instances they’ll create new platforms along with them.

📧 Feel free to flick me an email if you have any interesting news you’d like me to share with the FR community. I’m me@alantsen.com and @alantsen on the Twitters.

Ps. If you like what I’m doing with FR please feel free to share it on your favourite social disinformation channel of choice. Also, I’d appreciate if you forwarded this newsletter to a friend you think might enjoy it.

📰 News

As we all know, ‘embedded fintech’ is all the rage at the moment - which is just a fancy way of saying traditionally non-financial services companies offering financial services product. This piece is a solid rundown of how it looks in the context of verticalised challenger banking and more importantly it touches on the preconditions for it to work. Specifically, it notes:

As far as I can tell, you need at least two things to successfully run a vertical neobank program; proprietary customer acquisition in a specific segment, and differentiated financial benefits for the segment. This is not unlike co-branded cards of yesteryear. Programs like the Costco card and the United MileagePlus card worked really well for years because United had massive scale customer relationships through its loyalty program.

✋Bonus: This blog post is best read in tandem with the following two pieces from the Astra Finance blog: What does the future look like once we have a Fintech Platform? and Why haven’t we arrived at the AWS Era for Fintech?

🐜 Ant, Vanguard Target 900 Million Users With Robo Adviser

This week Ant Financial and Vanguard announced a JV to bring robo advice to Ant’s 900m customers. In what has to be a real distribution coup for Vanguard, the two companies will be going to market with a robo adviser which will recommend a portfolio chosen from 6,000 different mutual funds. According to the article, all transactions will be handled automatically and the robo adviser will also be able to help re-balance the user’s portfolio if required 🤖 💰

Distribution in China is a challenge if you’re not on one of the big platforms. In this regard, it makes a lot of sense from Vanguard’s perspective. Having said this, I can imagine that this will be one of many deals that Ant Finacial inks for distribution on their platform.

This is definitely a story worth keeping an eye on for all the China market entry strategists 👀

🔔 Chime pilots way to get $1,200 stimulus checks to users instantly after talks with Mark Cuban

Chime, one of the larger US challenger banks, is giving some of its customers early access to their stimulus payment. According to the article, Chime has randomly selected 1,000 customers and provided them with instant access to the $1,200 stimulus payment from the US government.

Although they’re potentially left holding the bag on this one if something goes wrong, it’s great to see fintech startups step up and contribute during these uncertain times. Over the coming weeks, I think we’ll see more of this kind of thing from fintech startups as they look to contribute - but also as they look to acquire customers while incumbent banks are left flat footed trying to figuring out how to WFH.

Worth noting, Mark Cuban isn’t all that responsible for this initiative 😂

📈 Microsoft announces Money in Excel powered by Plaid

This week Plaid announced that they’ve inked a deal with Microsoft to provide the bank feed for MS Money in Excel.

We all know the financial world is built on Excel (for companies and individuals alike) - remember that the OG PFM app is an Excel budget. I think this is a clever play from Plaid as they look to continue their growth globally. Although this has been available for a while through services like Tiller, this could really help cement Plaid as the go-to pipes for the transfer of financial information in the US.

💸 Peer-to-peer industry faces a rocky road ahead

To be honest, this has been an open question for a while in the P2P lending space: “What happens when the economy goes south?” This piece is an interesting look at both sides of this question.

It’s inevitably going to wipe some lenders out (and some are already halting/slowing down lending), but it could also present some big opportunities for some, as governments look at ways to inject money into the economy. Regardless, it’s one of the fintech verticals worth paying attention to as it will provide a good barometer as to where the industry is headed.

🤝 Open Banking Platform Tink Acquires Eurobits

Tink is probably one of the lesser-known open banking aggregation platforms out there, but this Scandinavian fintech has been quietly adding some big-name customers to the platform and recently raised a big round of funding - €90M at a post-money valuation of €415M - to fuel their international expansion. To help further push their global footprint they have acquired another player in the open banking space, Eurobits.

Eurobits is an interesting acquisition as they have extended out of Europe (they’re Madrid based) into South America, operating in 5 markets. This could be a clever strategic move to open up a market that Tink isn’t yet operating in.

🏦 Nubank shakes up Brazil’s banking bureaucracy

This is an interesting read about one of South America’s shining fintech stars, Nubank.

To be honest, this piece feels a little ‘light’. Having said this, it’s a good read if you haven’t heard of Nubank and it’ll give you a sense of why Brazil is such an interesting market for challenger banks.

🥶 From Cold Storage

💸 Minting Cash: how Square designed a product with no design at all

A great article from back in 2013 about the design of the Square Cash App. It’s a good read on the genesis of the product and is a great reminder that the best product experiences are simple, frictionless and delightful.

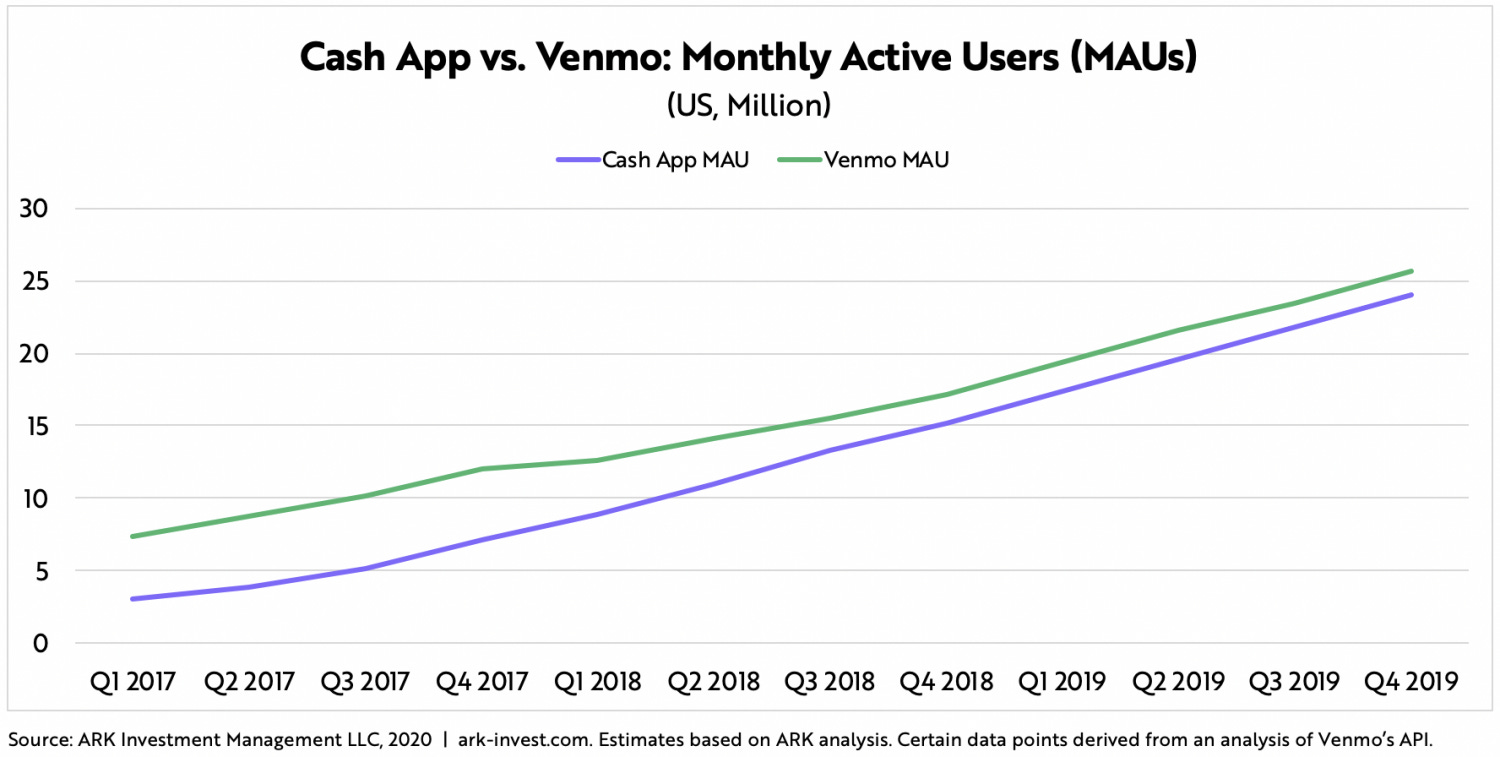

Bonus: Ark Invest wrote an interesting research piece on Square’s Cash App in February this year that is well worth a read. According to the piece, they estimate the Cash App may have crossed 24m MAUs as at December 2019 - which is kind of crazy.

If you’re a sceptic you’ll point at all the free money Square has been giving away to get people on the platform. If you’re into rap you’ll point to all the songs it’s been mentioned in (over 100 at last count) 📻 Regardless, it’s fairly impressive.

📚 Books To Read

This week I thought I’d recommend some fintech related books to keep you going through iso.

Digital Bank: Strategies To Succeed As A Digital Bank (Chris Skinner): This is an oldie, but a goodie. It’s well worth reading if you’re looking for a better understanding of why challenger banking is a thing.

The Sovereign Individual: How to Survive and Thrive During the Collapse of the Welfare State (James Dale Davidson and William Rees-Mogg): Ok, this book has become a bit of meme on Twitter - blame the SF VC set. Having said this, it’s a really interesting read on a number of fronts - everything from decentralisation through to the changing nature of regulation. Well worth picking up if you can find a cheap secondhand copy (I bought mine on Ebay).

Misbehaving: The Making of Behavioural Economic (Richard H Thaler): This last one is a little less fintech and more economics. Anyone who has read Thinking, Fast and Slow (or pretended to) will tell you what a hard slog it is. This is much more approachable and is just as relevant to understanding how behavioural economics can be applied in the real world.