Issue #67: Balance Secures The Bag, Bytedance Scales Back Its Fintech Aspirations And Defi Is Under The Regulator Microscope

Issue #67: Balance Secures The Bag, Bytedance Scales Back Its Fintech Aspirations And Defi Is Under The Regulator Microscope

👋 Hi, FR fam. I hope you’ve all had a great start to the week.

Thanks as always for being a subscriber 🙌 Also, welcome to all the new subscribers — glad to have you here and welcome to the FR fold.

If you like what I’m up to here at FR, please forward it to a friend or colleague. I’d really appreciate it!

Ok, without any further ado, let’s get into this week’s news from the world of fintech.

📣 The News Grab Bag

Early paycheck deposits might be coming to Robinhood ⚬ Open banking on hold in Brazil ⚬ Ikea’s parent company is investing $22.5m into BNPL startup Jifiti ⚬ PayPal might be launching a stock-trading product ⚬ Tinkoff is planning an expansion into the Philippines ⚬ The dawn of consumer crypto ⚬ Why paytech is the key to unlocking Africa's new free trade zone ⚬ Walgreens launches Scarlet ⚬ What went wrong with credit cards? ⚬ Canada's high-value payment system launches ⚬

📈 Notable Funding Announcements

It was another big week of funding announcements in the world of fintech. In total, 50 funding rounds were announced, totalling $2b.

⚖️ Balance Raises A $25 Million Series A⇢

B2B payment platform, Balance, last week announced a $25 Million Series A. Ribbit Capital led the round, with participation from Avid Ventures and existing investors Lightspeed Ventures, Stripe, Y Combinator Continuity Fund, SciFi VC and UpWest.

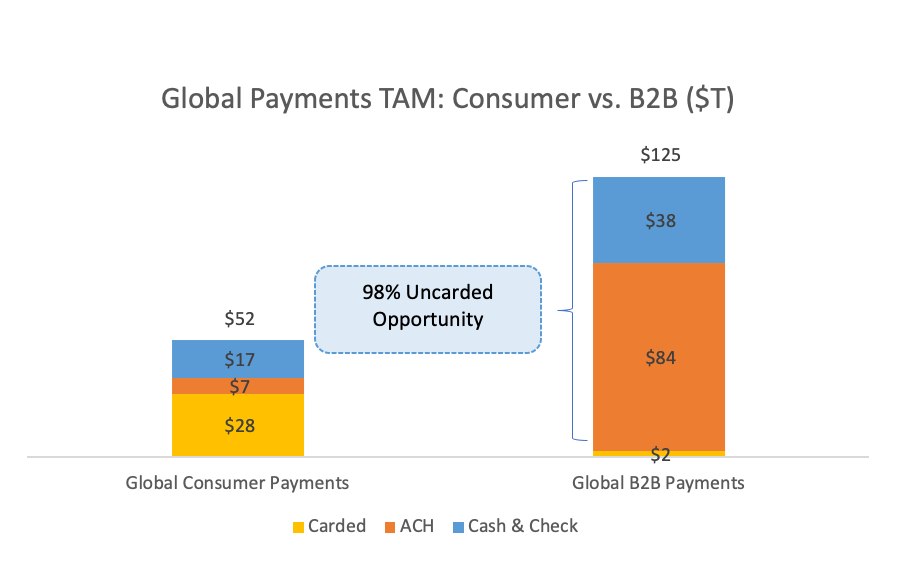

🤓 My Take: When looking at the payments sector, it’s easy to see it as a monolith. However, this is far from true. In fact, every segment of the payments industry is its own microcosm. In the case of B2B payments, it’s a world still dominated by offline payments. As Balance note in their press release announcing the round, “…92% of B2B transactions are still done offline, representing over $2T (more than 2x retail eCommerce)”. Although intuitively, it makes sense that the B2B payments sector is many times the size of retail payments, unless you deal with corporate payments on the daily it can be hard to appreciate how antiquated most of the tooling in this space really is.

If you’ve ever dealt with a procurement department, you’ll instantly understand the frustration that comes with making a payment B2B. If you haven’t, the TLDR is that it’s a segment riddled with Excel spreadsheet, pdf invoices and DD questionnaires still in MS Word — and all being sent via email. In a world where we’re all used to slick instant checkout experiences while shopping on Shopify powered sites and 1-click purchases on Amazon, the opposite is the case for B2B payments — they’re generally still clunky and often executed via wire or even cheques.

What’s deceptive about this segment is that the real issue most face isn’t about payments — it’s generally workflows and compliance that most need help with. Balance is a great example of a company trying to bring a more modern approach to the segment by offering a full-stack solution that provides everything from a modern checkout to automated reconciliations on the back end and even compliance for those who need to take their customers through a KYB process.

There’s no doubt that this is a crowded space, with incumbents on the left and a growing range of established ‘fintech’ companies (like unicorn AvidXchange) on the right, all making it a hard space to enter. Regardless of the intense competition for the corporate payments dollar, this latest round from Balance shows there is no shortage of cash ready to be thrown at companies trying to provide the segment with a more modern approach to payment management.

🕵️♂️ Checkr Raises $250m And Reaches A $4.6m Valuation ⇢

Last week Checkr announced a $250m Series E round of financing valuing the company at $4.6b. The round was led by Durable Capital, alongside new investors Fidelity Management and Franklin Templeton. The round also had participation from BOND Capital, Khosla Ventures, IVP, T. Rowe Price, Coatue, Accel, and Y Combinator.

🤓 My Take: Identity is a hot space in fintech/regtech at the moment. In Checkr’s case, they sit a little outside the usual KYC/AML/CTF companies you tend to see in the world of fintech. In fact, Checkr is focused on employee verification, providing their customers with the ability to check various records to verify an employee or candidate is who they say they are. Beyond this, they also allow employers to run a variety of checks to meet, for example, compliance requirements. As you’d expect, this all done through APIs.

Checkr rode the sharing economy wave when launched, and it quickly became the de facto product of choice for the bigger names in the sector. In fact, according to their website, they call Uber, Lyft, Instacart and Doordash customers.

In many ways, Checkr is part of a wave of identity companies that have realised that part of the challenge (and thus value in this segment) relates to aggregating up a disparate array of data and offering it up as an easy to consume API. More broadly, what goes under-discussed in the identity space is how the middleware players have really started to take hold. Once upon a time, a company would need to use a range of individual companies to verify each element of identity for a customer or employee. However, with the rise of identity middleware companies, it’s become easier than ever to use one set of APIs from a single startup to get all the information you need to verify someone is who they say they are. Watch this space.

☝️ Things You Should Know About

🕺 ByteDance To Sell Off Fintech Ops Following New Regulations ⇢

According to the article, ByteDance has announced that it plans to scale back its fintech aspiration in China following the recent clampdown by the Chinese government on the sector.

This pullback by Bytedance feels like it was inevitable and raises some broader questions about big tech companies operating in the fintech space.

It’s easy to discount this as an issue that is confined to the Chinese mainland — which, to be fair, has been aggressively reigning in tech companies more recently — but on a global basis, tech companies have been under fire. In fact, whether it’s Facebook having its initial launch of WhatsApp payments scuttled back in June 2020 or ApplePay more recently running into issues in Australia, it’s clear that many global regulators are becoming more concerned about the market power these tech behemoths wield. Regardless of whether you think it’s warranted or not, the idea of big tech companies operating financial services businesses seems less and less like an option.

It’ll be interesting to see what the rest of 2021 holds for big tech companies as they continue to look for ways to extend their reach in the payments space specifically and fintech more broadly.

🦄 Regulators Investigate Crypto-Exchange Developer Uniswap Labs ⇢

This week the WSJ reported that the SEC had begun a probe into Uniswap’s primary developer, Uniswap Labs, operations. Although the article was light on details and neither party has commented on the reported probe, the article suggests that the SEC may be looking into Uniswap’s market and investor services.

As the amount locked in defi last month passed $4b, along with the uptick in investor interest, attention from regulators is clearly also increasing. It’ll be interesting to see where this probe goes and whether it’ll be confined to Uniswap or whether it’ll have broader implications for the defi ecosystem.

🤔 Strategy Session: Frank Rotman Of Boutique Fintech VC QED Investors On Rebuilding Banking ⇢

In this great interview, Frank Rotman of QED drops some knowledge on investing in the world of fintech. I’m not going to spoil this one, but suffice to say, it’s well worth a read.

🎧 Podcast Recommendations

This week I thought I’d share two recent earning calls that provide some insights into what’s happening in the B2B fintech space.

→ nCino, Inc., Q2 2022 Earnings Call (Sep 01, 2021)

→ Bill.com Holdings, Inc., Q4 2021 Earnings Call (Aug 26, 2021)

❤️ Show Some Love For FR

📈 You can check out Radar, an open database of Australia's fintech ecosystem. You can find it here → 📡 SideFund Radar

📧 Feel free to reach out if you want to connect. I'm me@alantsen.com and @alantsen on the Twitters.

Ps. If you like what I'm doing with FR, please feel free to share it on your social disinformation network of choice. I'd also appreciate it if you forwarded this newsletter to a friend you think might enjoy it.

🙏 What did you think of this week's issue of FR?

I love it! ◌ I Like It ◌ Not Bad ◌ I Don’t Like It ◌ It’s Awful